Kareem Saleh

Are Bank Directors Worried Enough About Fair Lending?

Brought to you by FairPlay

Close

About the authors

Written by

Kareem Saleh

Bank directors and executives, be warned: Federal regulators are focusing their lasers on fair lending.

If your bank has not modernized its fairness practices, the old ways of doing fair lending compliance may no longer keep you safe. Here are three factors that make this moment in time uniquely risky for lenders when it comes to fairness.

1. The Regulatory Spotlight is Shining on Fair Lending.

Fair lending adherence tops the agendas for federal regulators. The Department of Justice is in the midst of a litigation surge to combat redlining. Meanwhile, the Consumer Financial Protection Bureau has published extensively on unfair lending practices, including a revision of its exam procedures to intensify reviews of discriminatory practices.

Collections is one area of fair lending risk that warrants more attention from banks. Given the current economic uncertainty, collections activities at your institution could increase; expect the CFPB and other regulators to closely examine the fairness of your collections programs. The CFPB issued an advisory opinion in May reminding lenders that “the Equal Credit Opportunity Act continues to protect borrowers after they have applied for and received credit,” which includes collections. The CFPB’s new exam procedures also call out the risk of “collection practices that lead to differential treatment or disproportionately adverse impacts on a discriminatory basis.”

2. Rising Interest Rates Have Increased Fair Lending Risks.

After years of interest rate stability, the Federal Reserve Board has issued several rate increases over the last three months to tamp down inflation, with more likely to come.

Why should banks worry about this? Interest rates are negatively correlated with fair lending risks. FairPlay recently did an analysis of the Home Mortgage Disclosure Act database, which contains loan level data for every loan application in a given year going back to 1990. The database is massive: In 2021, HMDA logged over 23 million loan applications.

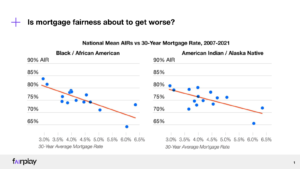

Our analysis found that fairness decreases markedly when interest rates rise. The charts below show Adverse Impact Ratios (AIRs) in different interest rate environments.

Under the AIR methodology, the loan approval rate of a specific protected status group is compared to that of a control group, typically white applicants. Any ratio below 0.80 is a cause for concern for banks. The charts above show that Black Americans have around an .80 AIR in a 3% interest rate environment, which plummets as interest rates increase. The downward slope of fairness for rising interest rates also holds true for American Indian or Alaska Natives. Bottom line: Interest rate increases can threaten fairness.

What does this result mean for your bank’s portfolio? Even if you conducted a fair lending risk analysis a few months ago, the interest rate rise has rendered your analysis out-of-date. Your bank may be presiding over a host of unfair decisions that you have yet to discover.

3. Penalties for Violations are Growing More Severe.

If your institution commits a fair lending violation, the consequences could be more severe than ever. It could derail a merger or acquisition and cause a serious reputational issue for your organization. Regulators may even hold bank leaders personally liable.

In a recent lecture, CFPB Director Rohit Chopra noted that senior leaders at financial institutions – including directors – can now be held personally accountable for egregious violations:

“Where individuals play a role in repeat offenses and order violations, it may be appropriate for regulatory agencies and law enforcers to charge these individuals and disqualify them. Dismissal of senior management and board directors, and lifetime occupational bans should also be more frequently deployed in enforcement actions involving large firms.”

He’s wasting no time in keeping this promise: the CFPB has since filed a lawsuit against a senior executive at credit bureau TransUnion, cementing this new form of enforcement.

How can banks manage the current era of fair lending and minimize their institutional and personal exposure? Start by recognizing that the surface area of fair lending risks has expanded. Executives need to evaluate more decisions for fairness, including marketing, fraud and loss mitigation decisions. Staff conducting largely manual reviews of underwriting and pricing won’t give company leadership the visibility it needs into fair lending risks. Instead, lenders should explore adopting technologies that evaluate and imbed fairness considerations at key parts of the customer journey and generate reporting that boards, executive teams, and regulators can understand and rely on. Commitments to initiatives like special purpose credit programs can also effectively demonstrate that your institution is committed to responsibly extending credit in communities where it is dearly needed.

No matter what actions you take, a winning strategy will be proactive, not reactive. The time to modernize is now, before the old systems fail your institution.

WRITTEN BY