Tom Wilson

Current M&A Trends and Implications

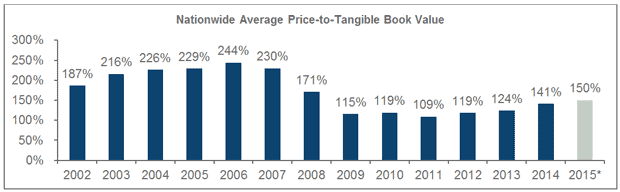

Bank and thrift merger and acquisition strength continued in the first quarter of 2015, with transaction volume essentially the same as the first quarter of 2014. A notable trend was the continued strengthening of transaction pricing, with 2015 transaction multiples at the highest levels since 2008.

Source: SNL Financial; transaction data through March 31, 2015

What is Driving Transactions?

Many of the factors driving the current M&A cycle have been well documented and remain largely unchanged—improving industry fundamentals, increased regulatory costs, net interest margin compression in a low rate environment, industry overcapacity, and economies of scale. While those themes have been playing out in various forms for several years, some additional themes are emerging that are significantly impacting the M&A environment:

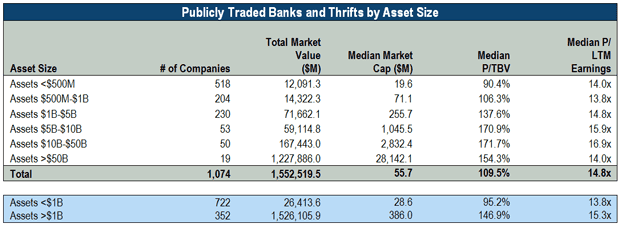

The advantages of scale are translating to a significant currency premium. For years we have seen a significant correlation between size, operating performance and currency strength. Lately, that trend has become a significant currency advantage for institutions with greater than $1 billion in assets and resulted in smaller institutions being constrained in their ability to compete for acquisition partners because of a weaker valuation. The chart below details current price to book and price to earnings multiples for publicly traded banks and thrifts based on asset sizes.

Source: SNL Financial; market data as of April 10, 2015

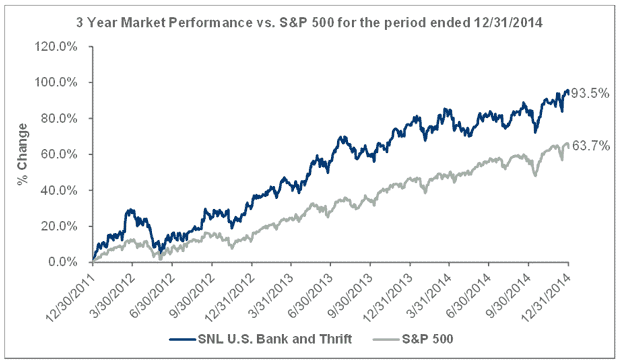

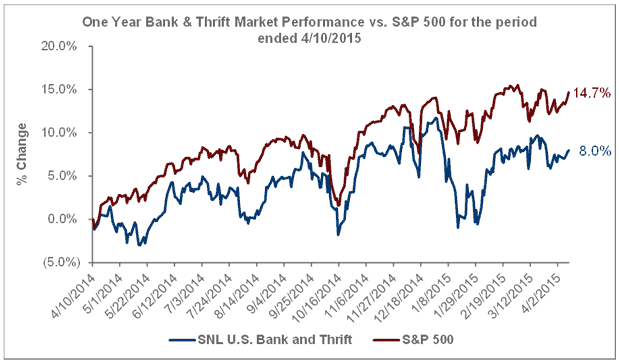

Net interest margin revenue challenges and uncertainty about the timing and magnitude of a Federal Reserve rate increase have placed pressure on bank stock performance. After recovering from the depths of the Great Recession, the banking industry experienced significant improvement in asset quality, capital levels, operating performance and earnings growth from 2011 to 2014. This translated to significant stock price performance, evidenced by banking stocks outperforming the overall market by nearly 30 percent on a cumulative basis during 2012 to 2014. However, beginning in early 2014, bank stocks have largely underperformed, mainly as a result of decelerating revenue and earnings growth and an uncertain outlook for Fed rate hikes. The result has been an alignment of buyers and sellers as buyers have utilized acquisitions to continue to increase revenues and sellers (smaller banks in particular) have concluded that a strategic partnership with a larger institution is the best method of delivering shareholder value.

Source: SNL Financial

Increasing M&A multiples have contributed to increased capital issuance. Increased transaction multiples is resulting in more goodwill creation, a higher likelihood of tangible book value dilution and a reduction in regulatory capital ratios. Acquirers are responding by issuing capital in what has been a favorable capital raising environment over the past several years due to a combination of strong price/earnings multiples and low interest rates. The banking industry has taken advantage of the favorable environment by issuing common and preferred equity and senior and subordinated debt. While some of the issuance has been focused on redeeming the government’s TARP/SBLF money, refinancing debt, and general corporate purposes, recent issuances have clearly been focused on merger activity. In reviewing offering documents, over half of issuers since the beginning of 2014 have indicated acquisition funding as a potential use of proceeds.

Conclusion

Merger and acquisition multiples have been increasing and 2015 will continue to be a favorable environment for M&A activity as the industry weighs the impact of potential rate increases and buyer and seller interests continue to align. Forward looking institutions have been raising capital to position themselves to be opportunistic buyers when strategic opportunities become available and sellers are taking advantage of a more favorable pricing environment.