Eric Solfisburg

The Significance of Size, Scale and Structure in BOLI

Brought to you by MassMutual

Close

About the authors

Written by

Eric Solfisburg

A bank is only as strong as its people, its client base and its assets. If your bank owns bank-owned life insurance (BOLI) among its assets, it’s important to know that your BOLI is only as strong as your BOLI insurance provider.

Bank executives familiar with the broad contours of BOLI may not be aware of other important considerations relative to their policies – considerations that may be unique to the product or the insurance carrier. Understanding these nuances can provide valuable insights into the resiliency, financial stability, and performance of your BOLI policy.

BOLI can be one of the most attractive assets on a bank’s balance sheet; in a low-rate environment with market volatility, it’s a good idea to consider including BOLI as part of a well thought-out asset strategy.

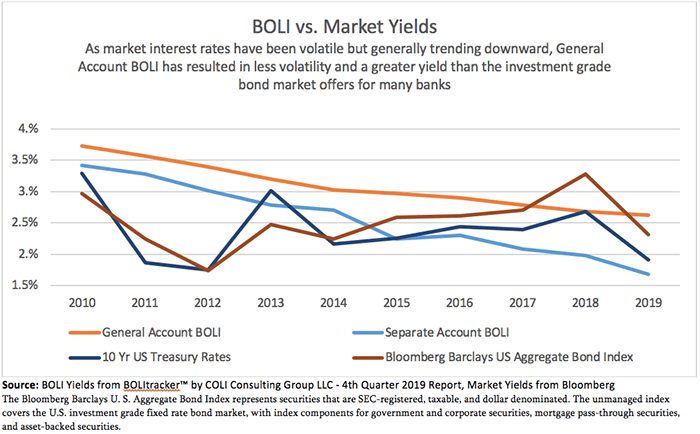

Two popular approaches for determining the crediting rates applicable to general account BOLI products are the “portfolio rate” and the “new money rate” methods. The new money rate method features crediting rates based on currently available securities, whereas portfolio-rate general account BOLI policies feature crediting rates based on the performance of an underlying seasoned portfolio. Crediting rates derived from well-diversified, low-turnover portfolios can serve as a form of hedge against volatile and lower market interest rates, while a new money rate product can benefit during a period of persistent and material increased market interest rates.

Each BOLI policy’s minimum guaranteed rate is backed by the credit quality, size and diversification of the issuing insurer’s investment portfolio. A portfolio’s resilience and financial strength are derived from the interplay between the core of investment-grade fixed income securities and holdings of potentially higher-yielding assets.

When it comes to BOLI, size and scale matter. Larger insurers are typically better equipped to purchase and provide exposure to a wider range of diversified assets, which contribute to the portfolio’s yield and BOLI crediting rates that banks value. Smaller carriers may not necessarily have access to the wide range of investment asset classes and market opportunities relative to larger carriers like MassMutual.

Beyond comparisons of the carriers’ investment portfolios and crediting rate approaches, there can be important differences when it comes to the insurers themselves. Because there is a limited universe of BOLI carriers, and their capabilities and strengths vary, each carrier brings unique types and levels of resources to bear. Each insurer offers banks different results based on its investment philosophy and expertise in managing the general investment account underlying its BOLI policies. Certain characteristics that differentiate insurers from each other include company structure, business mix, asset/liability management strategy, access to less widely available investment opportunities, and culture. The expertise, breadth and depth of experience of the insurer’s investment and business professionals should not be overlooked.

As a large mutual life insurer, MassMutual has a dedicated investments group that leverages our expertise in fixed income, equities and alternative assets, including real estate. The asset managers are insurance investors first and foremost, and they understand the business and the characteristics of the liabilities that the investments support.

The mutual structure enables insurers like MassMutual to take a long-term perspective. Decisions made with the next several decades in mind, not the next quarter, better align with the long-term nature of BOLI assets. This long-term view fuels our approach to maintaining financial strength and stability and drives our competitiveness.

Further, a carrier’s long-term market presence and commitment can be aided by diversification within its own subsidiaries, business lines and income streams. Just like in banking, having a diverse set of businesses can help reduce the economic sensitivity of an insurer. Diversified insurance carriers that offer a variety of solutions with varying characteristics are built to weather economic cycles and provide stability to a carrier. The combination of diverse income streams with a diversified pool of assets is a sound approach to help endure a wide variety of economic environments.

Banks have a variety of options when it comes to which BOLI insurer they select. Understanding each carrier’s structure, business mix, investment philosophy and market approach can inform executives’ choices as they embark on financial relationships that last decades.

Insurance products issued by Massachusetts Mutual Life Insurance Company (MassMutual), Springfield, MA 01111-0001.

WRITTEN BY