Rick Maroney

Senior Managing Director

Enter your email address and password below to gain access.

Rick Maroney is senior managing director at Hovde Group, LLC. He will help lead Hovde’s newest office in Toledo, Ohio and continue to serve depository institutions in the midwest and surrounding areas.

Mr. Maroney has a long history advising community banks on mergers and acquisitions, most recently with ProBank Austin, having started his career in 1984 with Austin Associates, LLC, the predecessor to ProBank. In addition to advising on more than 100 successful M&A transactions, he has extensive experience in preparing stock valuations, facilitating strategic planning and evaluating capital planning strategies, among other specialized services.

Mr. Maroney served as an instructor at the Stonier Graduate School of Banking and has appeared as a featured speaker at the Acquire or Be Acquired national conference, sponsored by Bank Director Magazine. He is licensed with the Financial Industry Regulatory Authority as a registered representative and holds the Series 7, 63 and 79 licenses.

While announced deal volume continues at a tepid pace, key drivers of M&A activity are starting to emerge. With more than 90 percent of the banking companies nationwide operating with assets of less than $1 billion, it is inevitable that consolidation will be concentrated at the community bank level. Six factors that point to a pick-up in M&A activity in this space are as follows:

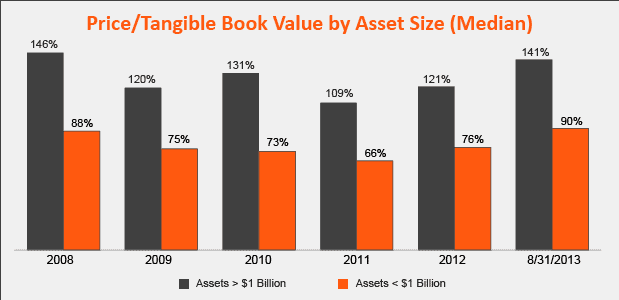

1. Bank equity prices are rising with an increasing valuation gap between small and large banks. Bank stocks overall have increased nearly 30 percent in 2013; however, banks with less than $1 billion in assets continue to trade at significant discounts compared to larger banks.

As the chart above indicates, the valuation gap has widened for larger banks, which enjoy a median 51 percentage point premium as of August 31, 2013. Larger banks can use this valuation advantage to present attractive deal pricing to smaller banks.

2. Very few FDIC-assisted transactions remain. Since 2008, 485 banks have failed representing nearly 7 percent of banking companies in the U.S., according to the Federal Deposit Insurance Corp. Essentially; FDIC-assisted transactions filled the void of traditional open-bank deals. With troubled bank totals dwindling and only a few significantly undercapitalized banks remaining, FDIC-assisted deals are diminishing. Acquisitive companies have moved on from this once lucrative line of business to evaluate more traditional deals.

3. Improved asset quality is leading to reduced credit marks. While merger discussions have occurred in recent years, the due diligence phase often brought deal negotiations to a screeching halt. With elevated credit marks (in some cases exceeding 10 percent), parties were unable to bridge the valuation gap. Over time, banks have made significant progress in reducing classified assets and writing down assets that more closely approximate fair value. With credit marks now modestly exceeding the target’s allowance for loan and lease losses, capital and book value can be preserved, which in turn, translates to more favorable deal pricing.

4. Several high profile deals have been announced at attractive premiums. Achieving certain benchmark pricing levels in M&A often is a catalyst for deal activity. Sellers are always looking for market information to help formulate a strategy on whether or when to sell. On the other side, buyers do not want to be perceived as overpaying, which is usually viewed in the context of pricing relative to other recent deals. Transactions like MB Financial’s acquisition of Cole Taylor Group at 1.82 times tangible book value and Cullen/Frost Bankers’ acquisition of WNB Bancshares at 2.84 times tangible book have already spurred discussion inside many boardrooms.

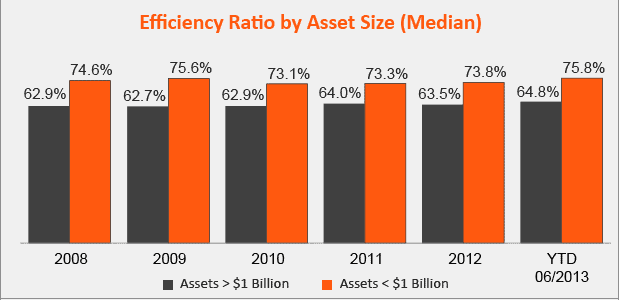

5. Economies of scale in the banking industry have never been more crucial. The need and desire to grow exists at virtually every institution. As the chart below indicates, efficiency ratios have remained consistently lower at larger banks.

Whether driven by regulatory costs, technology, marketing, pricing power, expanded lines of business/other revenue sources, larger banks appear to have clear performance advantages. This increasingly important trend will spur institutions to grow via acquisitions in order to spread certain fixed costs over a larger asset base and thereby improve operating efficiencies.

6. Mergers among community banks. None of the preceding points are intended to suggest that banks under $1 billion will not participate as buyers of other community banks. In fact, since 2010, banks of less than $1 billion in assets have announced or completed 280 acquisitions, comprising more than 41 percent of the deal activity during that period. A recent example of this type of deal involved Croghan Bancshares, which has $630 million in assets and is headquartered in Fremont, Ohio. Croghan is buying Indebancorp, which has$230 million in assets and is headquartered in Oak Harbor, Ohio. After considering other alternatives, Indebancorp chose Croghan, a larger community bank, as a partner. The deal was structured with 70 percent of the consideration in Croghan stock and priced at 134 percent of Indebancorp’s tangible book value. The deal value per share was 28 percent higher than Indebancorp’s stock trading price and cash dividends to Indebancorp shareholders will increase by almost 200 percent. On a pro forma basis, Indebancorp shareholders will own approximately 26 percent of Croghan’s shares following the deal.

Making M&A predictions is always challenging, but here at Austin Associates, we believe many community banks will make the decision to sell within the next few years. When M&A returns to full capacity, expect at least 300 transactions per year, or 20 percent consolidation of the industry within five years. Pricing will continue to increase, but do not expect to see pre-crisis multiples any time soon. Moreover, pricing will be highly dependent on the target’s unique profile (size and performance), as well as local and regional market factors.

Rick Maroney is senior managing director at Hovde Group, LLC. He will help lead Hovde’s newest office in Toledo, Ohio and continue to serve depository institutions in the midwest and surrounding areas.

Mr. Maroney has a long history advising community banks on mergers and acquisitions, most recently with ProBank Austin, having started his career in 1984 with Austin Associates, LLC, the predecessor to ProBank. In addition to advising on more than 100 successful M&A transactions, he has extensive experience in preparing stock valuations, facilitating strategic planning and evaluating capital planning strategies, among other specialized services.

Mr. Maroney served as an instructor at the Stonier Graduate School of Banking and has appeared as a featured speaker at the Acquire or Be Acquired national conference, sponsored by Bank Director Magazine. He is licensed with the Financial Industry Regulatory Authority as a registered representative and holds the Series 7, 63 and 79 licenses.