Mike Branton

Which Fee Income Camp Are You In?

Brought to you by StrategyCorps

Close

About the authors

Written by

Mike Branton

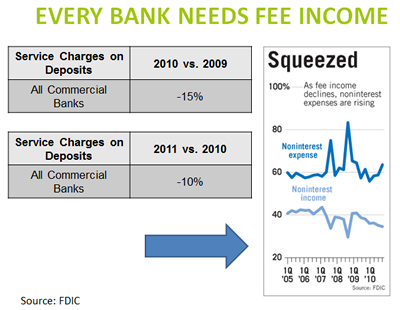

There’s no debate: Every bank needs more fee income, as do a lot of credit unions. The only debate is how a financial institution is going about meeting this need.

There’s no debate: Every bank needs more fee income, as do a lot of credit unions. The only debate is how a financial institution is going about meeting this need.

In StrategyCorps’ interactions with hundreds of banks and credit unions, we’ve identified three distinct camps in the need-more-fee-income challenge.

The Do-Nothing Camp. This group of financial institutions seems to be waiting for a sign that this recent decline in fee income will eventually pass. We’re not sure if that means they believe overdrafts are going to make a comeback or the Dodd-Frank Act will be repealed, or are simply in a state of denial over the fee income body blows the industry has been dealt. This camp nearly always seems to have fee income replacement on the to-do list, just not at or near the top, and oftentimes it is easily displaced by other things that are not as hard to deal with.

The “Fee-ectomy” Camp. A fee-ectomy is simply charging a fee for the same thing(s) that have been given away for free for a long time and with no corresponding additional value. As the name implies, the extraction of more fee income from customers on this unfair exchange of value basis is seemingly an easy and convenient way to generate more fee income. That is, until it starts causing significant heartburn for customers, provides negative headlines in the media and prompts the politicians to start politikin’. (Think $5 debit card fee.) This camp is comprised primarily of the larger banks that must feel the industry is basically an oligopoly, given their acceptance and commitment level to this fee income pricing strategy. Unfortunately, the by-product of the fee-ectomy strategy is an increased, or at least an ongoing, level of distrust for all banks that eventually breeds things like “bank transfer day” and unflattering customer reviews on Facebook.

The Back-to-Basics Camp. For years the industry talked about relationship banking, but never got around to doing much about it as the lucrativeness of overdrafts from free checking drowned out such discussion. Now smart financial institutions are genuinely trying to figure out what this means as a way to restore fee income by charging new fees for added value and also trying to cure the thousands of unprofitable accounts rather than firing them with arbitrary and value-less fees. This back to basics camp is approaching the fee income challenge by designing products with new features customers gladly pay for (for example, cell phone protection), marketing in a purposeful way that customers actually notice, creating better connections with customers through customized e-communication and reinforcing product education and sales training to frontline branch staff.

It’s pretty obvious which of the three camps will be the winner here (hint, it’s not the first two). But as those institutions that have adopted a back-to-basic strategy will attest, it’s not the passive way or the easy way. However, with clearly superior financial results and much happier customers, it is proving to be the right strategy for banks and credit unions that genuinely commit prioritized time and resources to addressing this issue.

WRITTEN BY