Jack Milligan

Editor-at-Large

Enter your email address and password below to gain access.

Jack Milligan is editor-at-large of Bank Director magazine, a position to which he brings over 40 years of experience in financial journalism organizations. Mr. Milligan directs Bank Director’s editorial coverage and leads its director training efforts. He has a master’s degree in Journalism from The Ohio State University.

With an apology to the late, great Samuel Beckett, the bank mergers and acquisitions market has begun to resemble the story line in Beckett’s Waiting for Godot where the two central characters—Estragon and Vladimir—spend the entire play waiting for a man named Godot, who never shows up. For the last few years, U.S. banks have been waiting anxiously for M&A activity to recover after the financial crisis of 2008, but the rebound has yet to show up.

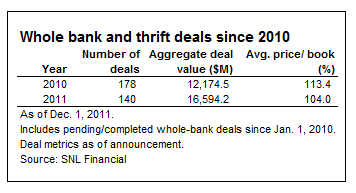

According to SNL Financial in Charlottesville, Virginia, there were 178 whole bank and thrift deals in 2010, with an average price-to-book valuation of 113.4 percent. Through Dec. 1 of this year, there were only 140 whole bank and thrift deals, for an average price-to-book valuation of just 104 percent—a clear indication that the bank M&A has cooled off. Unless something truly stupendous happens in terms of deal volume in what remains of 2011, this will turn out to be an even worse year for bank M&A than 2010.

According to SNL Financial in Charlottesville, Virginia, there were 178 whole bank and thrift deals in 2010, with an average price-to-book valuation of 113.4 percent. Through Dec. 1 of this year, there were only 140 whole bank and thrift deals, for an average price-to-book valuation of just 104 percent—a clear indication that the bank M&A has cooled off. Unless something truly stupendous happens in terms of deal volume in what remains of 2011, this will turn out to be an even worse year for bank M&A than 2010.

And based on the results of an email survey of independent directors, CEOs and other senior bank executives conducted by Bank Director and Crowe Horwath LLP in October, 2012 might not turn out to be much better. Of the survey’s approximately 225 respondents, 48.3 percent said they did not expect to make any type of acquisition—including a healthy bank, failed bank purchased through the Federal Deposit Insurance Corp., or branches—for the following 12 months, which would take us through October 2012.

“Activity is occurring, but it’s at a more modest level than it has been in the recent past,” says Rick Childs, director of assurance and financial advisory services at Crowe. “We are seeing some opportunistic buying, but buyers are being careful about what they take on.”

Of those respondents who said they would consider doing an acquisition, 36.6 percent expressed an interest in healthy banks, 26.8 percent in branches and 23.4 percent in an FDIC-assisted deal. Not surprisingly, there was little expressed interest—just 11.7 percent—in buying another bank’s loan portfolio, a probable sign that asset quality continues to be a concern throughout the industry. Childs says there are “some willing sellers out there,” including banks that have been unable to raise capital and are feeling the heat from their regulators, and banks that are worried about the rising cost of regulatory compliance following the passage of the Dodd-Frank Act and other recent regulatory initiatives.

Among likely acquirers, the top barrier to doing a deal—cited by 66 percent of the respondents—was lingering concern about the asset quality of potential targets. Other impediments included the “unreasonably high” pricing expectation of most potential sellers (56.9 percent), and the perceived risk of doing an acquisition in an uncertain economic environment (43.7 percent).

Also, when asked what the greatest barriers to selling their banks were, 69.3 percent responded that current pricing was too low.

“There is still a bit if a price gap between buyers and sellers,” says Childs. “Sellers understand that prices are down, but they’re still hoping for a higher price.”

Looking ahead to 2012, Childs expects there will continue to be an active market for FDIC assisted deals since there is still in excess of 800 banks that are in some kind of trouble. Many of those could end up being taken into receivership by the FDIC and either sold or liquidated. However, Childs does not look to see a significant increase in healthy bank acquisitions in 2012, even though organic growth will also be harder to come by, which normally would be a strong argument in favor of more takeover activity.

Instead, expect to see potential buyers wait for a stronger economy to lessen the risk of doing an acquisition, and for likely sellers to wait for better pricing.

“I think we’ll see a pretty sluggish market next year,” Childs says.

Just like Estragon and Vladimir in Godot, everyone’s still waiting.

Jack Milligan is editor-at-large of Bank Director magazine, a position to which he brings over 40 years of experience in financial journalism organizations. Mr. Milligan directs Bank Director’s editorial coverage and leads its director training efforts. He has a master’s degree in Journalism from The Ohio State University.