Amy McNulty

The Technological Imperative: Why Banks Need to Keep Up with Changing Consumer Demands

We live in a digital world where customers think less and less about the device they are using and more and more about the experience. Consumer technology is driving expectations. Customers are demanding real-time data, a consistent experience across all channels and a personalized relationship with their bank just as they do from their favorite shopping and online experiences like Amazon.com.

We live in a digital world where customers think less and less about the device they are using and more and more about the experience. Consumer technology is driving expectations. Customers are demanding real-time data, a consistent experience across all channels and a personalized relationship with their bank just as they do from their favorite shopping and online experiences like Amazon.com.

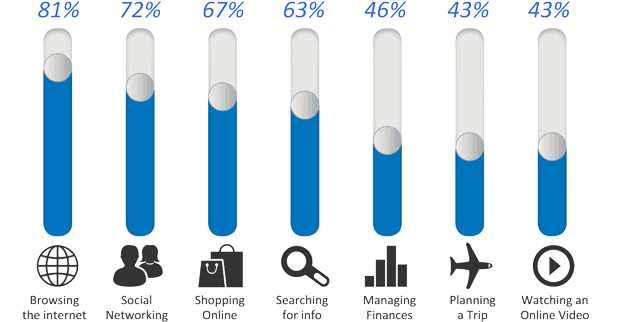

Today’s customers interact with financial institutions in a way that feels most comfortable and convenient for them, often beginning an activity in one channel, such as the branch, and moving between other channels, such as mobile phone and Internet banking, based on personal needs. According to the 2012 Google report, “The New Multi-screen World – Understanding Cross-platform Consumer Behavior,” 46 percent of people use multiple screens sequentially, by going back and forth, to manage their finances. The expectation of financial services providers is a single experience that delivers intuitive, relevant and individually tailored offerings.

Top Activities Performed Sequentially Between Devices

Source: “The New Multi-screen World – Understanding Cross-platform Consumer Behavior,” Google 2012

Compounding this issue is choice and ease of switching financial institutions. With advances in technology allowing the birth of digital banks not tied to any physical location, consumers have more choices than ever before. Consumers are more willing to use different institutions to meet specific needs, which makes the fight for share of wallet that much more important as bank channels proliferate and branch visits diminish. This means your customer experience is primarily defined now by an investment in banking technology.

Break Down Silos to Deliver a Holistic Experience that Transcends Channels

How can financial institutions adapt to meet these expectations? They can use a holistic approach to fully understand each of their customers and how they use technology. Traditionally, financial institutions built each customer touchpoint or channel in silos, often adding additional silos as new technology was introduced. Channels also frequently operate and are measured in isolation. This approach undermines the financial institution’s ability to tailor products and services to individuals, making a consistent user experience nearly impossible. Offers made in one channel (ATM), are declined by the customer only to be offered again in another channel (online) without the intelligent capability to know that the customer has turned down the offer already. Engagement and service opportunities are continually missed and customers become increasingly dissatisfied with the service and lack of personalization.

Leverage Data to Connect the Dots for Customers Across Touchpoints

The first step in laying the foundation for the omni-channel banking experience is in linking delivery channels such as bill pay, online, mobile, tablet and voice, along with the core through a common technical infrastructure. Financial institutions can then begin to leverage this valuable data to build a true customer profile, enabling more effective communications and driving loyalty through a more personalized customer experience. The technology and resources are available today to help financial institutions move in this direction. A growing number of service providers offer digital solutions tightly integrated across single platforms that deliver responsive, consistent experiences. And by using the data from these solutions coupled with the bank’s customer relationship management (CRM) tools, enabling online chat solutions, and leveraging the bank’s digital presence across the web and social media, banks are already well positioned to focus on improving the customer journey. This will not be an overnight process, but it will create tremendous opportunity as the future of banking unfolds.

Now is the time to get started. Begin with tracking where customers spend their time (phone, tablet, voice) and how they interact—to gain a better contextual understanding of customer preferences. By optimizing channels based on the nature of the interaction and customer preference, financial institutions will reap the benefits of the omni-channel experience.

Achieving the Omni-Channel Goal

Improving both customer experience and engagement is at the center of the omni-channel discussion. Brand loyalty will only be achieved by those that continually evolve to meet shifting customer expectations. Financial institutions must look at overall customer journeys and introduce consistent personalized interactions across all touchpoints. Continuing to operate in silos will cause significant loss as customers seek out other institutions that can provide the anytime, anyplace banking environment they demand.

Financial institutions now have viable technologies at their disposal to deliver innovative, tailored, touchpoint banking services. Community banks and credit unions or financial institutions of any size with limited resources can leverage the technology and data available to begin to apply this strategic approach. Those that respond now by working towards streamlined, integrated systems, a single customer view and optimal customer experience will ultimately get the edge over the competition and create lasting, profitable relationships with their customers.