Mike Branton

The Rise of the Subscription Society: Three Important Takeaways for Banks

Close

About the authors

Written by

Mike Branton

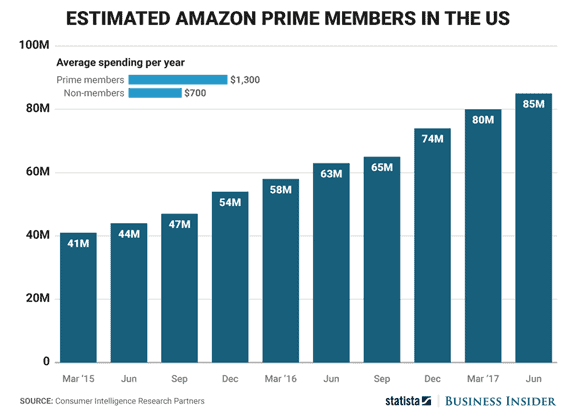

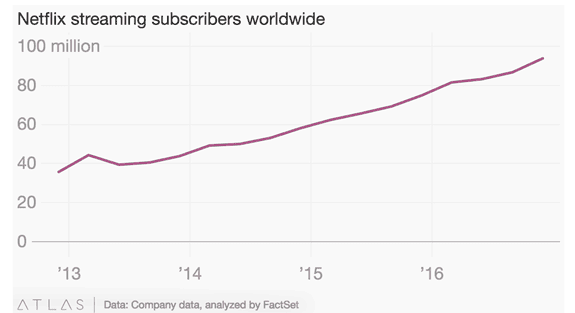

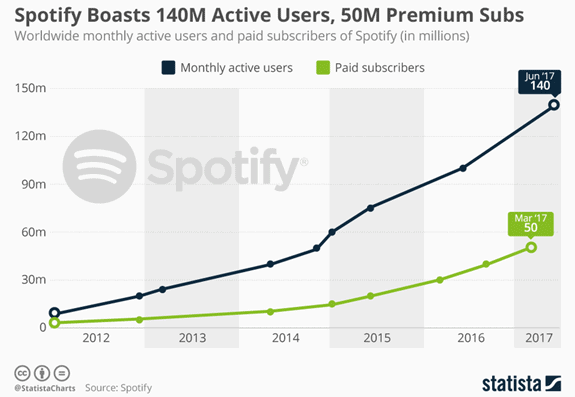

Subscription services are spreading like wildfire with huge leaps in subscription rates. Amazon Prime saw a 22 million household jump in 12 months, with 85 million Americans currently subscribed. Spotify started in 2011 with just 1 million subscribers and now, just 6 years later, has grown to 50 million paid subscribers. Then there’s Netflix, which just announced it has over 100 million total subscribers, about half of them in the U.S.

Subscription services are spreading like wildfire with huge leaps in subscription rates. Amazon Prime saw a 22 million household jump in 12 months, with 85 million Americans currently subscribed. Spotify started in 2011 with just 1 million subscribers and now, just 6 years later, has grown to 50 million paid subscribers. Then there’s Netflix, which just announced it has over 100 million total subscribers, about half of them in the U.S.

Success like this illustrates the subscription model isn’t merely a transactional structure, but has become the way for modern consumers to purchase (i.e. access to and use of product in reasonable installment payments as opposed to buying a product outright and owning it). Banks looking to make their products more attractive to consumers can use these companies’ successes as a model for their own service offerings.

So what makes the subscription-based model so compelling?

High Value, Low Cost

Subscription models provide a high amount of value at a lower cost than purchasing a product outright.

Take Amazon Prime, for example. Members are able to gain access to a large, discounted marketplace of products, free or discounted shipping that will deliver most purchases directly to their doors in under 48 hours, access to video streaming, music streaming, book libraries and personalized recommendations for just $10.99 per month (or discounted to $100 a year if they prepay in advance). These savings not only help the consumer save but also indirectly result in the development of healthier financial habits through Amazon’s network of discounts.

Spotify’s high value, low cost model offers the ability to pay a low monthly fee for access to unlimited music streaming as opposed to paying for each song individually or buying the DVD.

And a bank is taking notice of and acting on this subscription success. To make the Spotify subscription even more valuable, it has teamed with Capital One to reduce the monthly fee by 50 percent for 50 million potential customers, if the monthly payment source is a Capital One credit card.

Personalized Experience

Subscription services are also usually molded around the subscriber’s habits and preferences to deliver a personalized experience. Personalization ensures value is relevant to individual subscribers, as these services usually offer a wide library of products to ensure they’re universally appealing and accommodate various consumer needs.

This is another example where Spotify delivers. The service includes a so-called Discover portal dedicated to helping users find new music they would enjoy based on their streaming history and even delivers custom playlists on a weekly basis. Netflix and Amazon Prime also create a personalized list of recommendations and display them prominently on their websites so that users are immediately greeted by a relevant experience.

Banks have tremendous access to customers to provide relevant and timely offers and personalized deliverables to encourage engagement that goes beyond just traditional transactional experiences.

Convenience and Instant Access

In today’s technology-rich culture, consumers have come to expect instant access to the services, information and products they need. The subscription model was purposely built around providing convenience and immediacy.

In the not-so-distant past before Netflix, consumers would have to visit a video store or a movie theater if they wanted to watch a title on demand. More recently, they could order movies on demand from their cable or satellite providers, but this required purchasing titles individually and was often costly.

However, with video streaming services like Netflix, consumers now have a whole library of movies and TV shows to stream on demand whenever they want and they don’t have to purchase each title separately. Instead, they have access to Netflix’s full library for only $7.99 per month, which is about equivalent to purchasing one title.

Banks, of course, do have online and mobile banking products. What banks haven’t been able to do is fully monetize, with recurring revenue, this convenience and instant access. The next logical step is to find what new, non-traditional services can be instantly delivered through online and mobile platforms that customers will pay for.

The subscription model that delivers value, personalization and instant access can be successful for banks looking to build a more marketable brand and a larger and steadier stream of revenue. Amazon Prime, Spotify and Netflix are clearly examples of top performers of this model, but banks need to search out ways they can make their products more attractive and provide a value-rich, relevant and convenient experience for their customers.

WRITTEN BY