Emily McCormick

Vice President of Editorial & Research

Enter your email address and password below to gain access.

Emily McCormick is Vice President of Editorial & Research for Bank Director. Emily oversees research projects, from in-depth reports to Bank Director’s annual surveys on M&A, risk, compensation, governance and technology. She also manages content for the Bank Services Program. In addition to regularly speaking and moderating discussions at Bank Director’s in-person and virtual events, Emily regularly writes and edits for Bank Director magazine and BankDirector.com. She started her career in the circulation department at the Knoxville News-Sentinel, and graduated summa cum laude from The University of Tennessee with a bachelor’s degree in Spanish and International Business.

Banks increasingly face competition from outside the banking industry.

Banks increasingly face competition from outside the banking industry.

Facebook is already a licensed money transmitter, enabling the social media giant to process payments to application developers for virtual products. The retail juggernaut Wal-Mart Stores Inc. launched Bluebird in partnership with American Express Co. late in 2012 so users can direct deposit their paychecks, make bill payments, withdraw cash from ATMs and write checks. Customers also have access to mobile banking, which includes features like remote deposit capture and person-to-person (P2P) payments. As of August 2013, 1 million customers used Bluebird, according to Walmart Director of Communications Sarah McKinney. Wal-Mart’s Sam’s Clubs also offer small business loans through a non-bank Small Business Administration (SBA) lender. PayPal, which is owned by eBay, Inc., also has gotten into the business of P2P payments.

An audience survey of 120 bank directors and senior executives at Bank Director’s Growth Conference on May 1 found that many felt that their institutions are at least on par with their peers in the industry when it comes to innovation through technology, and just 17 percent said that their bank lags behind. However, the vast majority, at 91 percent, revealed concerns about non-banks entering financial services.

Community bankers aren’t alone in their concerns about competition from unregulated entities. Just days after the audience survey May 1, Jamie Dimon, CEO of JPMorgan Chase & Co., told the audience at the Euromoney Saudi Arabia conference in Riyadh that he sees Google and Facebook specifically as potential competition for the banking giant. Both offer services, such as P2P, that could chip away at income sources for banks. But the regulators could play a role in dampening these innovators’ ability to compete. “There’s no way that Google wants to be a regulated bank,” he said.

Perhaps Google and Facebook won’t pursue a future as regulated banks, but will partner with banks instead. CaixaBank, based in Spain, announced a partnership with Facebook on May 5 that will allow the bank’s customers to view account balances and transfers through their own Facebook profile or the bank’s Facebook page. Users can also make small donations to charities of up to 15 euros (about $20) to charities affiliated with the bank. CaixaBank plans to offer P2P payments through Facebook in the near future.

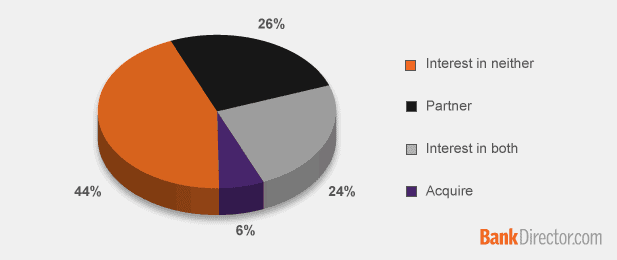

Half of the attendees surveyed at the Growth Conference said they would be open to a partnership with a financial technology firm. Wilmington, Delaware-based The Bancorp Inc., a financial services company with $4.7 billion in assets, offers private label banking to partners who sell services under the partner’s brand, including PayPal and Simple, which was recently acquired by Banco Bilbao Vizcaya Argentaria (BBVA).

Bill Roop, CEO and president of $1.1-billion asset Alpine Bank & Trust, headquartered in Rockford, Illinois, thinks the banking industry could see an increase in these types of partnerships. “You’re going to see a growing awareness of the different ways that you can touch a customer, and I think the industry has to be very open to partnering and working together to share the wallet…while also maximizing the benefit to the customer,” he says.

Regulations are often cited as constraints on a bank’s ability to innovate, but more attendees at the Growth Conference cited technology investment, at 42 percent, or the vendor relationship, at 31 percent, as greater barriers to innovation.

A little more than one-quarter of the audience blamed regulations for the lack of innovation in the industry. Regulation is just part of a banker’s life, says Roop. “Hire the appropriate individuals as you can, be sure you’re compliant with what the laws are, but our job is to serve the customers.”

The survey also found that one-third of attendees sit on bank boards with at least one member who has technology expertise, and almost half said that their board doesn’t have a technology expert but needs one.

As many community banks rely on core processors for customer-facing technology solutions such as mobile and online banking, the vendor can make or break an institution’s ability to innovate, and determining and investing in the right technology while still running an efficient institution can be a challenging balancing act for community banks.

“I’ve tried to weigh all these products and services out there. Yeah, I’d love to have all [of] these things but there’s a cost to that, and our cost is spread among $140 million in assets and two branches,” says Jim Marshall, CEO and president of blueharbor bank, which is based in Mooresville, North Carolina, and uses all lowercase letters in its name to convey a more contemporary approach to banking. “That’s one of the challenges of a small bank.”

Emily McCormick is Vice President of Editorial & Research for Bank Director. Emily oversees research projects, from in-depth reports to Bank Director’s annual surveys on M&A, risk, compensation, governance and technology. She also manages content for the Bank Services Program. In addition to regularly speaking and moderating discussions at Bank Director’s in-person and virtual events, Emily regularly writes and edits for Bank Director magazine and BankDirector.com. She started her career in the circulation department at the Knoxville News-Sentinel, and graduated summa cum laude from The University of Tennessee with a bachelor’s degree in Spanish and International Business.