Scott Gudmandson

Merger of Equals: Does 1 + 1 = 3?

Given today’s burdensome regulatory environment and complex business climate, many banks are evaluating different strategic alternatives as a means to grow. Mergers of equals (MOEs) are not always at the forefront of discussions when bank executives consider strategic alternatives, due to the social and cultural issues that can present roadblocks throughout the negotiation process.

Given today’s burdensome regulatory environment and complex business climate, many banks are evaluating different strategic alternatives as a means to grow. Mergers of equals (MOEs) are not always at the forefront of discussions when bank executives consider strategic alternatives, due to the social and cultural issues that can present roadblocks throughout the negotiation process.

It is vital to the success of a MOE that both parties come to terms on these issues early in the process to minimize the execution risk. When both parties of a MOE develop and align the structure of the transaction as well as the vision of the combined entity, MOEs can be executed successfully.

Historically, these issues have hindered MOE activity. Since 1990, MOEs have made up only 2.43 percent of total M&A transactions, reaching their peak (by number of deals) in 1998 before dropping off with the entire M&A market during the 2008 financial crisis. We are now seeing a resurgence in MOEs. As of Aug. 30, 2016, there have been seven MOEs this year making up 4.41 percent of total M&A activity in the community banking space. The banking industry has become increasingly more competitive in recent years, underscored by net interest margin compression as well as increased regulatory and compliance expenses. MOEs serve as an excellent alternative to cut costs, increase earnings, and gain size and scale.

In our eyes, successful MOEs cannot be forced; they are a marriage that must develop naturally between two institutions and their executives that have an amicable past with one another. They are most successful when the two banks’ philosophies and strategic visions align. While not every bank may be a fit for a MOE partner, we recommend that executives give consideration to merger opportunities, as a well-executed MOE can significantly enhance shareholder value.

MOEs present a significant opportunity to gain immediate size and scale that otherwise may not be achievable through small bank acquisitions. Achieving this size and scale will have a direct impact on the bottom line as the increasing regulatory burden can be spread across the firm while generating cost savings through the reduction of repetitive back office staff, overlapping branches, data processing contracts, and marketing expenses. Moreover, this will further enhance shareholder value through the pooling of talent and increased earnings stream generated by the bank, ultimately providing an opportunity for a higher takeout multiple in the event of a sale of the combined enterprise.

The market performance of MOE parties has reflected the positive impact that MOEs can have. When comparing the stock performance since January 2010 of both the accounting acquirer and accounting target (a merger of equals always has, for accounting purposes, an acquirer and a target), on average they have both outperformed their peers, beating the SNL US Bank & Thrift index three months after the announcement by 1.9 percent and 3.7 percent, respectively. Moreover, the pro forma bank has outperformed the SNL US Bank & Thrift index at both one- and two-year time frames after the mergers have closed; the average stock price change of the pro forma bank one-year post closing is 15.9 percent compared to 8.9 percent for the SNL US Bank & Thrift index and over two years is 22.0 percent compared to 13.3 percent.

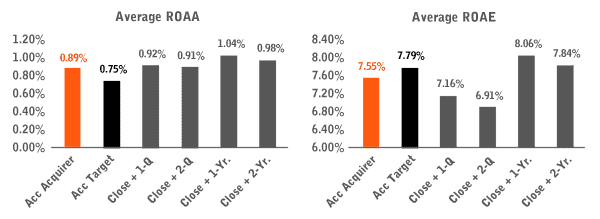

Additionally, the combined enterprise has also performed well financially. The average pro forma bank has increased both return on average assets (ROAA) and return on average equity (ROAE) one and two years after the transaction closing.

Average Pro Forma Bank Before and After a Merger of Equals

Source: S&P 500 Market Intelligence

Note: ROAA and ROAE for acquirer and target are as of the quarter prior to transaction announcement. Includes select MOE transactions from 1/1/2010 to 8/28/2016 in which the accounting buyer is publicly traded; includes 12 transactions. Transactions in which ROAA and/or ROAE are not available for specific time periods are excluded from average ROAA and/or ROAE calculations.

When a MOE is well executed it can bolster earnings, gain scale, increase efficiency and improve products and practices, ultimately creating a stronger combined institution. In these cases, the whole is greater than the sum-of-the-parts and 1 + 1 = 3.