Kiah Lau Haslett

Banking & Fintech Editor

Enter your email address and password below to gain access.

Kiah Lau Haslett is the Banking & Fintech Editor for Bank Director. Kiah is responsible for editing web content and works with other members of the editorial team to produce articles featured online and published in the magazine. Her areas of focus include bank accounting policy, operations, strategy, and trends in mergers and acquisitions.

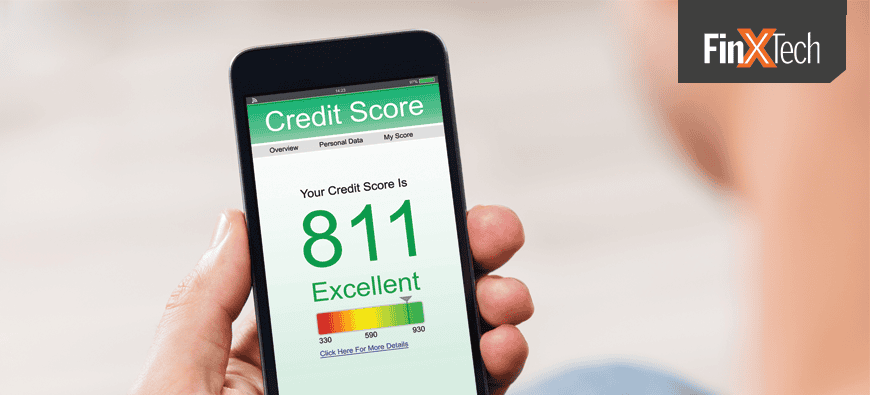

One community bank is using a fintech to deepen lending relationships with customers and help them monitor and improve their credit score.

One community bank is using a fintech to deepen lending relationships with customers and help them monitor and improve their credit score.

Watford City, North Dakota-based First International Bank and Trust wanted to offer customers a way to proactively monitor their credit and receive monthly or incident-related alerts about any changes – without needing to use external vendors, granting external access to accounts or even paying for it. It chose to partner with SavvyMoney, which provides customers with their credit scores and reports alongside pre-qualified loan offers from within the bank’s online and mobile apps.

The fruits of the relationship were one reason the fintech was awarded the Best Solution for Loan Growth at Bank Director’s 2020 Best of FinXTech Award in May. CommonBond, a student loan refinancer, and Blend, which offers banks an online, white-label mortgage processing solution, were also finalists in the category.

In exploring how it could help customers improve their credit score and manage their finances, First International knew some customers were already using similar services through external websites. But the $3.6 billion bank wanted to convey that it had invested time and IT resources to ensure SavvyMoney’s validity, accuracy and status as a trusted partner, says Melissa Frohlich, digital banking manager. The SavvyMoney feature takes about 45 seconds to activate once a customer is logged in, and the customer experience is the same in the mobile app or website.

“From the fraud standpoint, we definitely recommend to our customers that … they use SavvyMoney because it’s free to them,” Frohlich says. “Especially with all the breaches that happen, it’s a good way for them to self-monitor their credit.”

The bank also uses the platform to share specialized credit offers along with a customers’ loan information and credit score, which it crafts using public records and extends based on internal criteria. It has launched two credit card balance transfer offers since rolling out the product two years ago. The fintech offers First International a way to “slice and dice” data to truly target customers with customized offers, as opposed to “throwing out a fishing line and hoping someone bites,” she says.

Launching the offers takes “very little” time to implement and consists of updating a term sheet, whipping up bank graphics and sending out a simple email blast. The first offer netted more than $190,000 in balance transfers – all from one email campaign.

“It was just very, very little work for us with pretty significant impact, without a ton of manpower or money that we had to put into it,” Frohlich says.

The balance transfer offer included messaging about how much customers would save with the new interest rate. If First International wanted to offer auto loan refinancing, it could input different rates based on the year of the vehicle and loan term.

First International was drawn to SavvyMoney in part because it had an existing relationship with a variety of core providers. That’s key, given that SavvyMoney connects to a bank’s core to pull in personal customer information from online and mobile banking sources. And because it would be sharing customer data, First International spent several months conducting due diligence, combing through SavvyMoney’s system and organization controlsreports and speaking with both its core and the fintech.

Frohlich says the actual implementation took about a month and was as straightforward as flipping a switch to activate the capability in customer accounts. She continues to work with her representative at SavvyMoney to add or change loan offers.

“They have probably the best integration that I’ve seen with Fiserv from a third party or a fintech, out of any other product that Fiserv doesn’t own,” she says. “The actual implementation was the best that I’ve ever taken part in.”

SavvyMoney can also integrate with the bank’s new loan platform that was slated for a March launch, a fact that Frohlich didn’t know when the bank selected either. Loan applications submitted through SavvyMoney will feed into the software’ auto decision-making.

“That will be a game changer for us, then we will heavily start doing more promotions,” she says.

Even after the bank switched cores, it has been able to keep SavvyMoney given its vendor relationships with other cores. “There have been other solutions, that now that we’re moving to a different platform, that I could consider,” Frohlich says. “But to be honest, our experience has been so great with SavvyMoney that I have no reason to look elsewhere.”

Kiah Lau Haslett is the Banking & Fintech Editor for Bank Director. Kiah is responsible for editing web content and works with other members of the editorial team to produce articles featured online and published in the magazine. Her areas of focus include bank accounting policy, operations, strategy, and trends in mergers and acquisitions.