Bart Narter

It Takes More Than a Village Redux: The Decline of the Community Bank

Overview

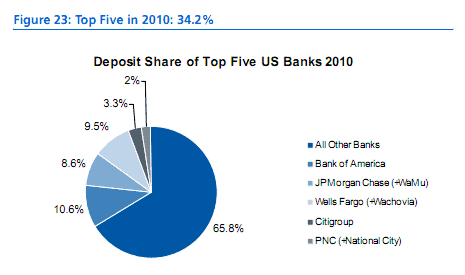

In 2009, Celent predicted the continuing decline of banks below $500 million in assets due to extreme disadvantages in efficiency ratios. These predictions did come to pass. Today the top five banks in the United States now have nearly 35 percent of all domestic deposits. Is this concentration good for the bankers? Is it good for the financial system? Are too many banks simply too big to fail?

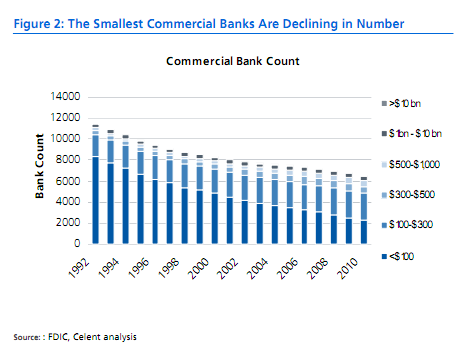

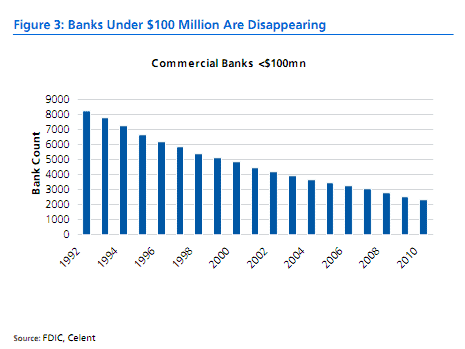

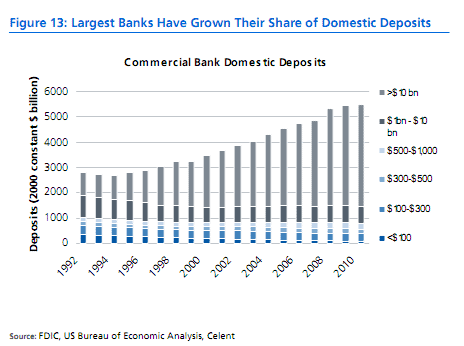

The smallest banks in the United States are disappearing. Their count dropped by 5,967 from 1992 to 2010. Their deposit base has dropped even more quickly. Running a bank requires a certain amount of scale, and that floor is rising due to increasing regulatory requirements, channel support, and product support.

Clearly banks below $100 million in assets are under this floor, and banks between $100 million and $300 million are quickly finding themselves at serious cost disadvantages. Banks between $300 million and $500 million started losing deposits in the last two years.

On the other side of the scale, the big are getting bigger very quickly. Where the top five banks had 11 percent of all deposits in 1995, this number had grown to 34 percent of deposits in 2010. FDIC regulations prohibit a bank from having more than 10 percent of all deposits, which puts the theoretical maximum at 50 percent for the top five.

The top two are already near, at, or beyond that limit. The concentration of the top five banks will increase incrementally, within these constraints.

Celent still sees a role for the banks over $10 billion in assets (and even over $500 million in assets) outside the top five largest banks. They will continue to thrive at the expense of the smallest banks. On the smaller end of the $10 billion and above spectrum, these banks will offer personal service while having sufficient scale to support their IT and operations infrastructure. On the larger end of the scale, these banks are likely to be a bit more efficient than the top five, with slightly less complex offerings. This part of the US banking environment is poised to thrive in the upcoming years.

Banks under $100 million in assets will decline in number by about 6 percent per year; those from $100 to $300 million should decline by about 2 percent per year. The future for the smallest banks in the United States is not bright for the next few years.

For more information about this report, review this press release from Celent.