Naomi Snyder

Editor-in-Chief

Enter your email address and password below to gain access.

Editor-in-Chief Naomi Snyder is in charge of the editorial coverage at Bank Director. She oversees the magazine and the editorial team’s efforts on the Bank Director website, newsletter and special projects. She has more than two decades of experience in business journalism and spent 15 years as a newspaper reporter. She has a master’s degree in journalism from the University of Illinois and a bachelor’s degree from the University of Michigan.

Everyone asks Ben Plotkin the same question: When are things going to settle down in banking?

Good question.

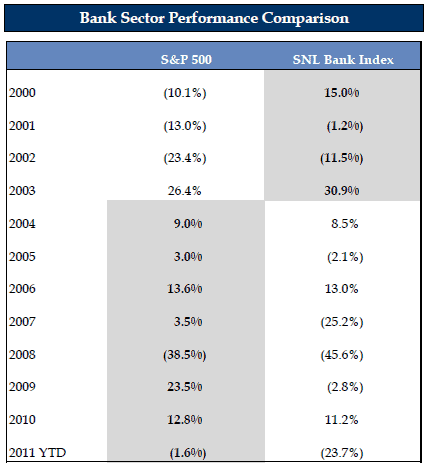

The balance sheet crisis has passed, said the executive vice president and vice chairman of investment bank Stifel Nicolaus Weisel. Asset quality has improved. Capital levels are strong. Yet valuations remain low for banks. Banks, in fact, have underperformed the broader market for the last eight years.

And the headwinds in the industry remain substantial: banks are getting hit with increased regulatory costs and rules that lower fee income, just at a time when interest rates are low.

“It makes it a bit of a challenge to convince your friends and neighbors to invest in banks,’’ Plotkin said, speaking at Bank Director’s annual Bank Executive and Board Compensation Conference in Chicago last week.

The third quarter showed that small and large banks were both able to improve profitability by reducing their provisions for loan losses, tied to improving assets on their books, as well as reducing expenses. Large-cap banks in general reduced expenses by 7.6 percent in the quarter compared to 3.4 percent for small and mid-cap banks, according to Stifel.

However, everything in banking is being reset at a “new normal,’’ as banks must keep higher levels of capital and better quality capital on their books in the midst of a low-growth environment, while earning less in fees for everything from debit cards to overdraft.

“It does affect earnings power,” Plotkin said. “In the past, banks could rely on operating leverage to solve those problems. You had expenses, but you saw growth. Right now, because of the economy, it’s difficult to see that operating leverage.”

Plotkin also warned the crowd of nearly 300 attendees at the conference to remember “shadow banks” such as Internet banks, broker-dealers and money market mutual funds are all competing with banks and thrifts for depositors.

Meanwhile, the top five banks in the nation have gone from controlling 22 percent of the deposit market share to 40 percent between the year 2000 and 2011.

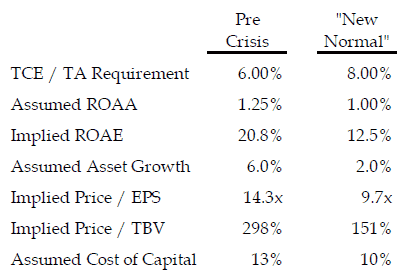

Plotkin presented a hypothetical model, where a bank that once enjoyed a return on average assets of 1.25 percent and annual asset growth of 6 percent now will get 1 percent return on average assets and 2 percent annual growth. That same bank can expect to see its stock formerly valued at nearly 3 times tangible book value fall to 151 percent.

So there lies the rub. Banks are under pressure in terms of future growth, low profitability and difficulty raising capital, as well as competition, but few of them have been sold during the financial crisis, which has slowed M&A activity down to a trickle.

Plotkin said everyone knows there’s a coming wave of consolidation in the industry, but it is still hampered by low valuations on the part of buyers, regulatory uncertainty and lingering credit concerns. Seller expectations for better pricing also are putting a crimp on acquisitions.

“If all the buyers are trading at 150 percent of book, why would they pay you 250 percent of book for your company?” Plotkin said.

When M&A activity will pick up is anyone’s guess.

“Tipping points aren’t things we can predict,’’ he said. “I’ve been doing this for 30 years but I can’t tell you.”

Source: SNL Financial, market data as of Nov. 2, 2011

Source: SNL Financial, market data as of Nov. 2, 2011

Illustrative Mode: The “new normal” for a hypothetical bank

*TCE/TA means tangible common equity/tangible assets. ROAA means return on average assets. ROAE means return on average equity. EPS means earnings per share and TBV means tangible book value.

Source: Stifel Nicolaus Weisel

Editor-in-Chief Naomi Snyder is in charge of the editorial coverage at Bank Director. She oversees the magazine and the editorial team’s efforts on the Bank Director website, newsletter and special projects. She has more than two decades of experience in business journalism and spent 15 years as a newspaper reporter. She has a master’s degree in journalism from the University of Illinois and a bachelor’s degree from the University of Michigan.