Christa Steele

Blockchain Information Series: Why Blockchain Matters

FinXTech Advisor, Christa Steele, has created a four part series to educate our community about how blockchain is changing the transaction of digital information, its implications and the players who are shaping this technology. Below is Part Two of this series.

I recently attended Bank Director’s annual Acquire or Be Acquired Conference in Phoenix, Arizona. Richard Davis, the CEO of U.S. Bancorp, gave the keynote address. As always, Richard captivated the audience with his presentation on not only leadership but where he sees the future of banking heading and why education–internally and in the boardroom–is so mission critical. Two of his slides urged for board education on things such as digital identity, big data, IoT, cognitive computing/artificial intelligence and biometrics/security. On both of these slides, Richard mentioned blockchain. Here is a brief snapshot of one of Richard’s slides about where we are as an industry now and five-plus years from now:

- Tokenization, EMV, mobile

- SDA, real time payments

- ISO 20022

- Open API

- Identity Management

- Distributed Ledger Technology/Blockchain

- Internet of Things (IoT)

- Machine Learning

Richard’s presentation affirms blockchain’s relevancy in the new digital world. Keeping pace with these trends is imperative, as the way we operate today is quickly changing due to competition, technology and capability.

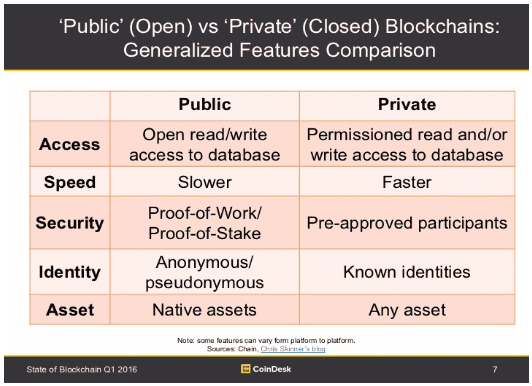

Let’s review what we have learned so far about blockchain. We can liken blockchain to an assembly line with a series of blocks, or a database maintained over a network of computers connected via a cryptographically secure peer-to-peer exchange. This information can be stored utilizing a public or private network in which the movement of digital (tokenized) assets are tracked and recorded.

Public networks are accessible to anyone without any restrictions. Data stored on a public network is encrypted and visible to all network parties. The network does not have any intermediaries and instead relies on the individual parties to verify transactions and record data on the network.

Two ideal examples of a public network:

- County Records in which deeds of trust are recorded in a highly antiquated and manually-driven process. Today, title reports and other recorded information is readily available to the public. With blockchain, parties can buy and sell an unencumbered real estate asset independent of the need for title company involvement or title insurance. Think about it_why are we paying for title insurance? It’s to insure against errors. As a commercial banker by background, I see huge time savings and process improvement potential in how we source, collect information, underwrite, approve, document, fund and record commercial real estate loans utilizing blockchain technology.

- Secretary of State Filings used to establish a new business entity and for securing a new deposit, loan or investment account. Today, new businesses are required to complete a largely manually driven application process riddled with errors. Think about the potential of blockchain if secretary of state filings were hosted in a public network accessible by the banks to integrate directly in to the new account opening process, loan application, funding, boarding and recording process.

Private networks are permissioned networks for those entities that have been granted access. Private networks are limited to allowing only trusted or known parties access to the network. A private network would be financial institutions transacting with one another or on behalf of a mutual client. This private network may also be utilized by regulatory bodies to monitor and/or govern the behavior of the financial institutions.

Each party, whether it is public or private, maintains a key or “address” where the digital asset is located on the network. This key grants restriction or permission to the asset and to the asset transfer.

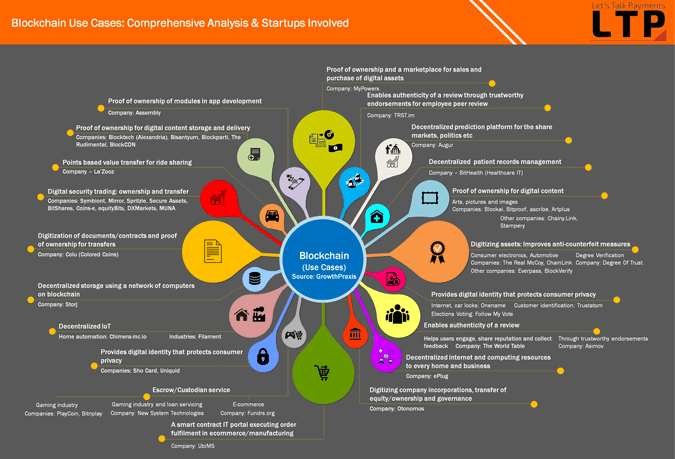

There are many blockchain use cases being explored in the financial sector. Other examples include, but are not limited, to:

- In the debt and derivative markets, providing faster clearing and settlement, increased transparency of counter party risk and reduced trade settlement errors of syndicated loans and repurchase agreements.

- Corporate bonds can be automated for not only payment calculation but for payment coupons and redemption.

- Automating credit default swaps for processing and monitoring to insure greater transparency and improve post-trade settlement efficiency.

Distributed ledger technology still hosts a lot of unknowns yet to be determined as to how public vs. private blockchains will be utilized and governed in the financial sector. We know that regulation is not going to be eliminated. It will be important to determine what level of human interaction is required as opposed to what can be automated and decisioned in the public or private network. Governance, operational structure and network security are top of mind for all parties involved.

What other applications does blockchain support?

As you can see, Blockchain (aka distributed ledger technology) has expanded far beyond that of the financial sector. Companies such as Kaiser Permanente, Cargill Foods, Toyota and many others have hired teams to evaluate their vertically integrated infrastructures and determine how this technology can enhance client experience, timing to market and efficiency.

For more information specifically related to the financial sector, I encourage you to read FINRA’s January 2017 article, “Distributed Ledger Technology: Implications of Blockchain for the securities industry.” We will explore who the players are, specific use cases and discuss the challenges and opportunities of adopting this technology in subsequent articles.