Vinay Bhaskar

Best Practices to Achieve True Financial Inclusivity

Brought to you by Scienaptic

Close

About the authors

Written by

Vinay Bhaskar

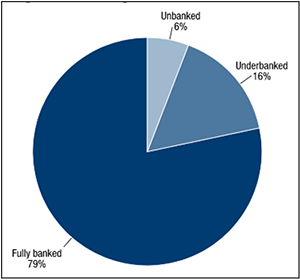

According to the Federal Reserve’s report on the economic well-being of U.S. households in 2019, 6% of American adults were “unbanked” and 16% of U.S. adults make up the “underbanked” segment.

Source: Federal Reserve

Source: Federal Reserve

With evolving technological advancements and broader access to digital innovations, financial institutions are better equipped to close the gap on financial inclusivity and reach the underserved consumers. But to do so successfully, banks first need to address a few dimensions.

Information asymmetry

Lack of credit bureau information on the so-called “credit invisible” or “thin file” portions of unbanked/underbanked credit application has been a key challenge to accurately assessing credit risk. Banks can successfully address this information asymmetry with Fair Credit Reporting Act compliant augmented data sources, such as telecom, utility or alternative financing data. Moreover, leveraging the deposits and spend behavior can help institutions understand the needs of the underbanked and unbanked better.

Pairing augmented data with artificial intelligence and machine learning algorithms can further enhance a bank’s ability to identify low risk, underserved consumers. Algorithms powered by machine learning can identify non-linear patterns, otherwise invisible to decision makers, and enhance their ability to screen applications for creditworthiness. Banks could increase loan approvals easily by 15% to 40% without taking on more risk, enhancing lives and reinforcing their commitment towards the financial inclusion.

Financial Inclusion Scope and Regulation

Like the Community Reinvestment Act, acts of law encourage banks to “help meet the credit needs of the communities in which they operate, including low- and moderate-income (LMI) neighborhoods, consistent with safe and sound banking operations.” While legislations like the CRA provide adequate guidance and framework on providing access to credit to the underserved communities, there is still much to be covered in mandating practices around deposit products.

Banks themselves have a role to play in redefining and broadening the lens through which the customer relationship is viewed. A comprehensive approach to financial inclusion cannot rest alone on the credit or lending relationships. Banks must both assess the overall banking, checking and savings needs of the underbanked and unbanked and provide for simple products catering to those needs.

Simplified Products/Processes

“Keep it simple” has generally been a mantra for success in promoting financial inclusion. A simple checking or savings account with effective check cashing facilities and a clear overdraft fee structure would attract “unbanked” who may have avoided formal banking systems due to their complexities and product configurations. Similarly, customized lending solutions with simplified term/loan requirements for customers promotes the formal credit environment.

Technology advancements in processing speed and availability of digital platforms have paved the way for banks to offer these products at a cost structure and speed that benefits everybody.

The benefits of offering more financially inclusive products cannot be overstated. Surveys indicate that consumers who have banking accounts are more likely to save money and are more financially disciplined.

From a bank’s perspective, a commitment to supporting financial inclusivity supports the entire banking ecosystem. It supports future growth through account acquisition – both from the addition of new customers into the banking system and also among millennial and Gen Z consumers with a demonstrated preference for providers that share their commitment to social responsibility initiatives.

When it comes to successfully executing financial inclusion outreach, community banks are ideally positioned to meet the need – much more so than their larger competitors. While large institutions may take a broader strategy to address financial inclusion, community banks can personalize their offerings to be more relevant to underserved consumers within their own local markets.

The concept of financial inclusion has evolved in recent years. With the technological advancements in the use of alternative data and machine learning algorithms, banks are now positioned to market to and acquire new customers in a way that supports long-term profitability without adding undue risk.

WRITTEN BY