John Maxfield

Freelancer

Enter your email address and password below to gain access.

John Maxfield is a freelance writer for Bank Director magazine. He was previously the senior banking specialist at The Motley Fool. He regularly writes for Bank Director magazine and BankDirector.com. His work has been syndicated widely to national publications including USA Today, Time and Business Insider, and he’s been a regular guest on CNBC. John has a bachelor’s degree in economics from Lewis & Clark College and a juris doctorate from Southern Methodist University. He’s a licensed attorney in the State of Oregon.

It’s hard not to be intrigued by the merger between BB&T Corp. and SunTrust Banks. After all, it’s the biggest deal in banking since the megamergers of the financial crisis.

It’s hard not to be intrigued by the merger between BB&T Corp. and SunTrust Banks. After all, it’s the biggest deal in banking since the megamergers of the financial crisis.

The rationale for the deal is simple. “While each one of us are doing fine today, we both recognize that to move forward with the best premiere financial institution, we needed additional scale so that we can make the technological investments necessary to provide the digital platform and other technological support features,” said BB&T Chief Executive Officer Kelly King in an interview after the announcement.

Sitting next to King, SunTrust CEO Bill Rogers emphasized a different point-namely, that the combination is a merger of equals. “I think the key of the ‘E’ is that it’s ‘E,’” said Rogers. “We’re confident that we are going to have the best M.O.E. possible, because we’re off to the best start possible.”

The anticipated economics of the deal are attractive. The combined company is expected to emerge with a 51 percent efficiency ratio, compared to ratios of 57 percent and 60 percent for BB&T and SunTrust, respectively. And the banks’ combined return on average tangible common equity is projected to increase to 22 percent, up from 20 percent at BB&T and 17 percent at SunTrust.

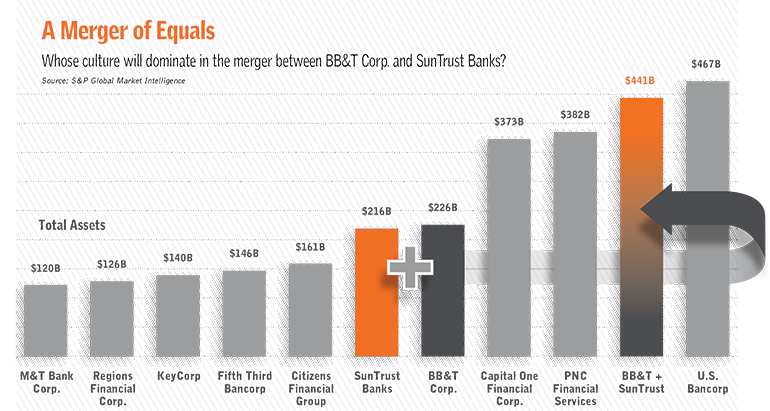

The challenge will be smoothly integrating banks of roughly equal size, particularly given that each bank has more than $200 billion in assets. Together, they will make the second largest superregional bank in the country, behind only U.S. Bancorp.

The most important element, as King acknowledged, will be merging the banks’ cultures.

As King sees it, the companies are almost identically aligned in this regard. “If you look at SunTrust, for example, their mantra, their cultural mantra is lighting the way to financial well-being,” said King. “At BB&T, we say we will make the world a better place to live. What better way to make the world a better place to live than to light the way to financial well-being with the challenges so many people in our world have today.”

This makes the task seem easy enough. Yet, it glosses over the fact that BB&T has one of the most unique cultures in the banking industry. Its mission, purpose and value statements are inspired by the writings of philosophers like Aristotle. Its officers must read Ayn Rand’s book, “Atlas Shrugged.” And when one listens to King at the bank’s annual investor day, it seems more like a spiritual event than a bank gathering.

It remains to be seen how the banks will marry their cultures. But if culture really is a competitive advantage, then one would be excused for presuming that, based on the banks’ performances in recent years, BB&T’s will carry the most weight.

There are bankers today, many of whom have advanced deep into their careers, who have never witnessed a rising rate environment from the inside of a bank. The last time interest rates were on the ascent was the summer of 2006-what seems like a lifetime ago.

There are bankers today, many of whom have advanced deep into their careers, who have never witnessed a rising rate environment from the inside of a bank. The last time interest rates were on the ascent was the summer of 2006-what seems like a lifetime ago.

It is hard to overstate the significance of this.

The banking industry has undergone fundamental changes over the past decade. Partially obscured by the recovery from the financial crisis has been the proliferation of digital banking, which is rewiring the way consumers access, spend and manage their money.

And now, just as bankers have begun to absorb the significance of these changes, they’re faced with the added challenge of a rising rate environment.

There are certainly benefits to higher rates. Higher rates and lower taxes propelled the banking industry to record profits in 2018, for instance, as banks earned a wider margin on their loans and kept a larger share of it.

But there’s a downside to higher rates as well-two downsides, actually.

The first is credit risk. Rising rates don’t lead directly to higher loan losses, but they do lead indirectly to credit problems, as nine out of the past nine recessions were all precipitated by rising rates.

The second is interest rate risk. This has traditionally been associated with the fear that a bank’s cost of funds will exceed the yield on its earning assets. This was the proximate cause of the savings and loan crisis in the 1980s, as thrifts were limited at the time to investing in 30-year fixed-rate mortgages that earned 8 percent or so, while runaway inflation caused their cost of funds to climb into double digits.

This precise set of facts is less troublesome now, as bank balance sheets are more diversified and, in many cases, indexed to prevailing rates. But there are still complications. The main issue today is whether rising rates will cause a reallocation of deposits in the industry, from small banks to big banks and fintechs.

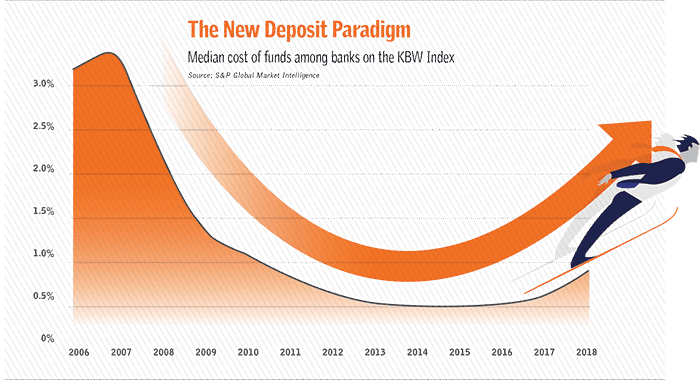

This is why bankers are watching their cost of funds so carefully. As you can see in the chart above, the median cost of funds among banks on the KBW Bank Index ticked up gradually in 2016 and 2017, from 35 to 51 basis points, and then climbed more rapidly last year, to 79 basis points.

The Federal Reserve’s enthusiasm for rate hikes seems to have tempered of late, which should dampen the rise of deposit costs. But bankers shouldn’t lose sight of the fact that there’s still a long way to go before rates normalize on an historical basis.

John Maxfield is a freelance writer for Bank Director magazine. He was previously the senior banking specialist at The Motley Fool. He regularly writes for Bank Director magazine and BankDirector.com. His work has been syndicated widely to national publications including USA Today, Time and Business Insider, and he’s been a regular guest on CNBC. John has a bachelor’s degree in economics from Lewis & Clark College and a juris doctorate from Southern Methodist University. He’s a licensed attorney in the State of Oregon.

Bank Director’s annual Bank Services Membership Program combines Bank Director’s extensive online library of director training materials, conferences, our quarterly publication, and access to FinXTech Connect.

Become a Member

Our commitment to those leaders who believe a strong board makes a strong bank never wavers.