Lukas Hohl

Realign Your Bank’s Operating Model Before It’s Too Late

Brought to you by Synpulse

The banking industry and its underlying operating model is facing pressure from multiple angles. The advent of new technologies including blockchain and artificial intelligence have started and will continue to impact the business models of banks.

The banking industry and its underlying operating model is facing pressure from multiple angles. The advent of new technologies including blockchain and artificial intelligence have started and will continue to impact the business models of banks.

Meanwhile, new market entrants with disruptive business models including fintech startups and large tech companies have put pressure on incumbent banks and their strategies. A loss of trust from customers has also left traditional banks vulnerable, creating an environment focused on the retention and acquisition of new clients.

In response to looming industry challenges, banks have begun to review and adapt their business models. Many banks have already adjusted to the influence of technology, or are in the process of doing so. Unfortunately, corresponding changes to the underlying operating models often lag behind technology changes, creating a strong need to re-align this part of the bank’s core functions.

So what does “re-align” mean from an IT architecture point of view?

Impact on System

In order to keep up with the fast-paced digital innovation, investments have largely focused on end-user applications. This helped banks to be seen as innovative and more digital friendly. However, in many cases these actions led to operational inefficiencies and there are several reasons why we see this.

One is a lack of integration between applications, resulting in siloed data flow. More often, though, the reason is the legacy core, which does not allow seamless integration of tools from front to back of an organization. Further, M&A activity has led many banks to have several core legacy systems, and often these systems don’t integrate well or exist with multiple back-end systems that cater to a specific set of products. This complicates the creation of a holistic view of information for both the client and financial advisor.

There are two ways of addressing the above-mentioned challenges to remain successful in the long-run:

- Microservice driven architecture

- Core Banking System modernization

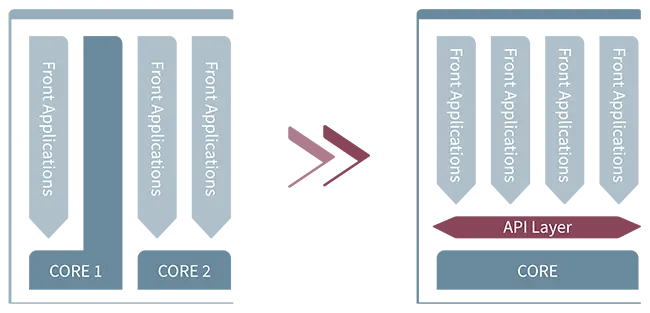

Microservice-driven architecture

Establishing an ecosystem of software partners is important to be able to excel amid rapid innovation. Banks can’t do all the application development in house as in the past. Therefore, a microservice-driven architecture or a set of independent, yet cohesive applications that perform singular business functions for the bank.

The innovation cycles of core banking systems are less frequent than innovation cycles for client- and advisor-facing applications. To guarantee seamless integration of the two, build up your architecture so it fully supports APIs, or application programming interfaces. The API concept is nothing new; however, to fully support APIs, the use of standardized interfaces will enable seamless integration and save both time and money. This can be done through a layer that accommodates new solutions and complies with recent market directives such as PSD2 in Europe.

Core Banking System Modernization

Banks are spending a significant amount of their IT budget on running the existing IT systems, and this allows only specific parts go into modernization.

A simple upgrade of your core banking system version most likely won’t have the desired impact in truly digitizing processes from front to back. Thus, banks should consider replacing their legacy core banking system(s) to build the base layer of future innovation. This can offer new opportunities to consolidate multiple legacy systems, which can reduce operational expenditures while mitigating operational risks. In addition, a core banking replacement allows for the business to scale much easier as it grows.

A modern core banking system is designed and built in a modular way, allowing flexiblity to decide whether a specific module will be part of the existing core or if external solutions will be interfaced instead, resulting in a hybrid model with best-of-breed applications in an all-in-one core banking system.

Investing In Your Core Can Save You

Core banking system modernization and adoption of the microservice-driven architecture are major investments in re-aligning a bank’s operating model. However, given the rapid technological innovation cycles, investments will pay off in improved operational efficiency and lower costs.

Most importantly, re-aligning the operating model will increase the innovation capabilities, ultimately resulting in a positive influence on the top line through better client experiences.