Ben Lewis

Managing Director and Global Head of Sales

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.

As bank management teams turn the page to 2022, a few themes stand out: Their institutions are still flush with excess liquidity, loan demand is returning and the rush of large M&A is at a fever pitch.

But the keen observer will note another common theme: hedging. Three superregional banks highlighted their hedging activity in recent earnings calls.

These banks use derivatives as a competitive asset and liability management tool to optimize client requests, investment decisions and funding choices, rather than be driven by their associated interest rate risk profile.

Why do banks use derivatives to hedge their balance sheet?

Why are some banks hesitant to use swaps?

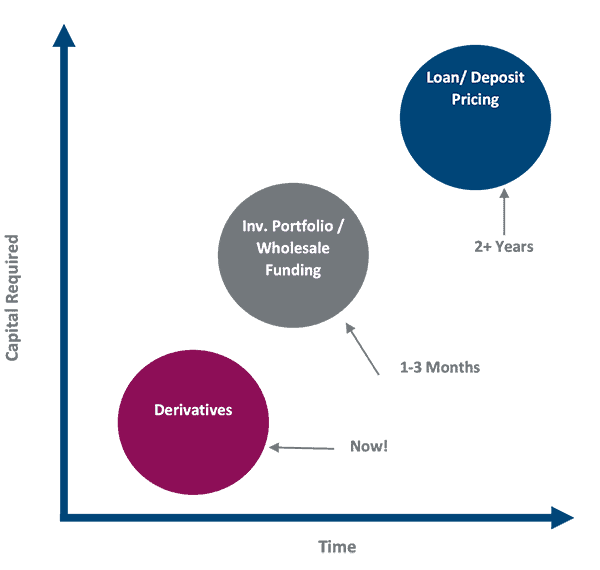

For banks that have steered clear of swaps – believing they are too risky or not worth the effort – an education session that identifies the actual risks while providing solutions to manage and minimize those risks can help separate facts from fears and make the best decision for their institution. The reality is community banks can leverage the same strategies that these superregional banks use to enhance yield, increase lending capacity and manage excess liquidity.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.