Dave DeFazio

Executive Vice President – Strategy and Solutions

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Dave DeFazio is Executive Vice President – Strategy and Solutions at StrategyCorps. Armed with a passion for banking strategy, Mr. DeFazio has found great success and satisfaction in exploring the intersection of data, marketing, and technology. Mr. DeFazio’s extensive financial services experience and continuous research in the field help him ensure that each product and service meets the needs of today’s financial institutions.

Mr. DeFazio leads and manages the company’s direct sales efforts while working directly with financial institutions to design, build and implement a variety of checking solutions. Mr. DeFazio is a highly sought-after speaker who has shared thought leadership on innovations in financial technology, retail banking, mobile banking, customer engagement, product and customer profitability, product design, bank marketing and changing consumer behaviors in an increasingly mobile-centric world.

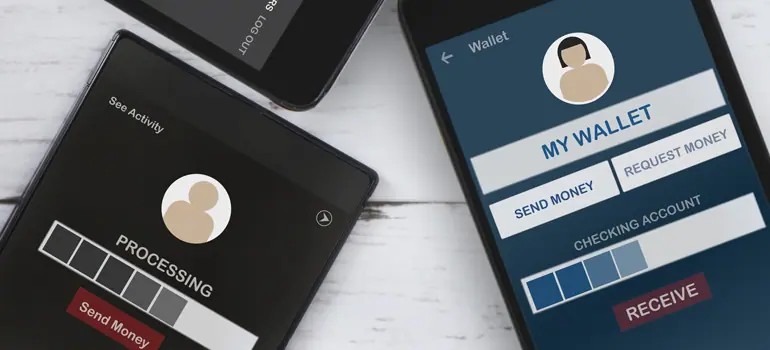

The banking industry saw one of the biggest technological developments of the year in June with the introduction of Zelle, a peer-to-peer (P2P) payments app now offered by over 30 of the leading U.S. financial institutions. Participating are some of the biggest names in banking, such as JPMorgan Chase & Co., Wells Fargo & Co., Bank of America Corp., Citigroup and Capital One Financial Corp., as well as many smaller banks through partnerships with leading payment processors.

The banking industry saw one of the biggest technological developments of the year in June with the introduction of Zelle, a peer-to-peer (P2P) payments app now offered by over 30 of the leading U.S. financial institutions. Participating are some of the biggest names in banking, such as JPMorgan Chase & Co., Wells Fargo & Co., Bank of America Corp., Citigroup and Capital One Financial Corp., as well as many smaller banks through partnerships with leading payment processors.

The ability to make quick and easy peer-to-peer payments across banks has existed for a few years now, although most banks haven’t had this capability. In fact, PayPal’s Venmo has overwhelmingly dominated the peer-to-peer payments space. The introduction of Zelle marks the first bank-backed response to Venmo, and thus, the banking industry’s most significant attempt to capture some P2P market share from third-party technology providers.

It’s only been a few months and already Zelle has had a clear influence on the industry. Bank of America recently reported around 11 million P2P transfers made in 2Q2017, reflecting an 89 percent increase from 2016. Overall P2P payments users have also increased by 39.5 percent from the start of this year, likely in part due to Zelle.

It remains to be seen whether Zelle will be able to trump Venmo’s popularity, but in either case, its launch can teach banks a few valuable lessons about their own service offerings.

The Appeal of Venmo

Venmo was launched independently in 2009 and later acquired by PayPal in 2013 after gaining considerable traction, especially among millennials. Perhaps one of the reasons it saw so much popularity with this demographic is the built-in social elements that appeal to millennials’ desire to connect with friends online and to “see and be seen.” Users can view friends’ transactions through a newsfeed, send personalized transaction messages and even integrate with Facebook so it’s easier to locate friends.

Another major reason for Venmo’s popularity is its ease of use. The app now supports text and voice control integration, seamlessly aligning with how users are already using their phones by allowing them to send or request payments simply by sending a text or dictating the command to their phone.

The Introduction of Zelle

With the wild popularity of Venmo, many banks realized they were being blown out of the water when it came to peer-to-peer payments. In response, Bank of America, Wells Fargo, and JPMorgan Chase teamed up with payments technology company Early Warning to begin developing their own app that could facilitate payments between their customers.

While Zelle has the disadvantage of its network being limited to participating banks, the app introduces a few compelling benefits that make it a true contender for Venmo. Primarily, there’s a feeling of security that comes with an app associated with the bank itself, since users won’t have to submit sensitive data into a third-party platform.

With transfer between banks using Zelle, users will also be able to receive money instantly instead of having to wait a few days for the transaction to process through Venmo. They’ll also enjoy a more seamless banking experience as Zelle is accessed through the host bank’s existing mobile banking app so customers making P2P transactions can also complete other banking tasks within the same platform.

What Banks Can Learn

Ultimately, the launch of Zelle isn’t just a lesson for banks to offer innovative technology. More importantly, it’s a reminder for them to keep an eye on technology companies and the way they’ve influenced bank customers, or else they may be missing out on valuable business opportunities.

So why did banks wait so long to present a competitive solution to Venmo? Even though many noted the popularity of Venmo years ago, they might have waited because there was no straightforward way to generate profit in the P2P space.

However, providing a relevant, convenient and user-friendly experience is of the utmost importance for banks, as that’s what continues to attract and drive business—and ultimately, does generate a profit. Given how prevalent technology has become to consumers’ daily lives, building technology into this experience is not only essential but expected.

Regardless of whether or not Zelle comes out on top, its launch is only a positive for banks. The innovations Venmo and similar companies have introduced have forced banks to reprioritize and modernize their services, focusing more on building deeper, more valuable relationships with their customers than simply on profits. And with those relationships, profits will come.

Dave DeFazio is Executive Vice President – Strategy and Solutions at StrategyCorps. Armed with a passion for banking strategy, Mr. DeFazio has found great success and satisfaction in exploring the intersection of data, marketing, and technology. Mr. DeFazio’s extensive financial services experience and continuous research in the field help him ensure that each product and service meets the needs of today’s financial institutions.

Mr. DeFazio leads and manages the company’s direct sales efforts while working directly with financial institutions to design, build and implement a variety of checking solutions. Mr. DeFazio is a highly sought-after speaker who has shared thought leadership on innovations in financial technology, retail banking, mobile banking, customer engagement, product and customer profitability, product design, bank marketing and changing consumer behaviors in an increasingly mobile-centric world.