Ben Lewis

Managing Director and Global Head of Sales

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.

Twenty years ago, there were 8,000+ banks; today there are less than 5,000, but competition hasn’t slowed.

Not only are banks competing with other banks for loans, they are also competing for investor dollars. There’s pressure to grow and to do so profitably. It is more important than ever that banks compete for, and win, loans.

Competing for the most profitable relationships requires banks to meet borrower demand for long-term, fixed-rate debt. But that structure and term invites interest rate risk. What can banks do? What are their competitors doing?

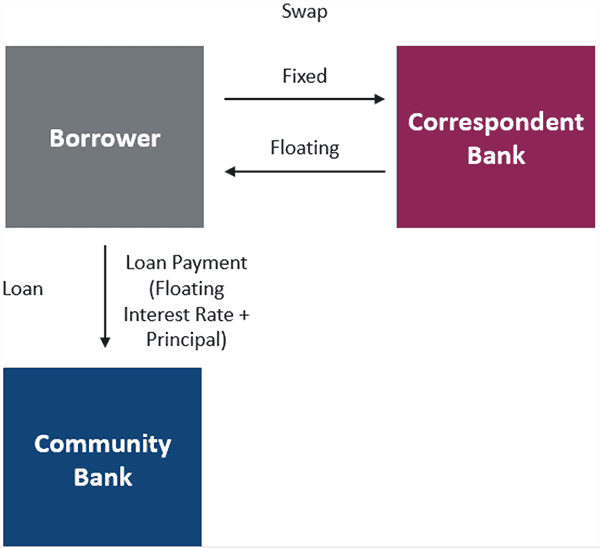

Banks commonly use derivatives to meet customer demand for fixed-rate loans, but opt for different approaches. The majority of banks choose a traditional solution of offering swaps directly to borrowers; however, some community banks choose to work with correspondent banks that offer indirect swaps to their borrowers.

With indirect swaps, the correspondent bank enters an interest rate swap with the borrower – sometimes called a rate protection agreement. The borrower is party to a derivative transaction with the correspondent bank; the community bank is not a direct party to the swap.

Indirect swaps are presented as a simple solution for meeting customer demand for long-term fixed-rates, but community bankers should consider the three C’s of indirect swaps before using this type of product: credit, cost and customer.

Credit

A swap is a credit instrument that can be an asset or liability to the borrower, which means the correspondent bank requires security. The correspondent bank accomplishes this by requiring a senior position in the loan credit. In a borrower default, the correspondent bank has the first lien on the loan collateral.

In practice, the community bank makes the correspondent bank whole for the borrower’s swap liability. This means the community bank has an unrecognized contingent liability for each indirect swap.

Additionally, due to the credit nature of swaps, the correspondent bank must agree to the amount of proceeds, or the loan-to-value at which the bank lends. This has real-world implications for banks as they compete for loans.

Cost

While there are no out-of-pocket costs associated with putting the borrower into a swap with a correspondent bank, there are costs embedded in the swap rate that drives up the cost for the borrower and could potentially make the bank uncompetitive. These costs are often opaque – and can be significant.

Customer

A colleague of mine refers to indirect swaps as “swaps on a blind date.” It’s a funny but apt way of putting it. The borrower enters into a derivative with a correspondent bank that they have no relationship. And the borrower is accepting unsecured exposure as well: if the correspondent bank defaults and owes the borrower on the swap, they have no recourse except as an unsecured creditor.

A common theme of the three C’s is control. With indirect swaps, the community bank cedes control of the credit, they cede control of the cost of the swap and they cede control of the relationship with their customer. That’s why the majority of banks choose to offer swaps directly to their customers. Doing so allows them to manage the credit, including loan proceeds, and doesn’t subordinate the bank’s credit to a third party in the case of a workout. It allows the bank to own the pricing decision and control the cost of the swap to the borrower, making the bank’s loan pricing more competitive. It allows the bank to keep all aspects of the customer relationship within the institution.

Offering swaps to borrowers also opens the door for banks to use swaps as a balance sheet risk management tool. In this context, derivatives are an additional tool for the bank to manage interest rate risk holistically.

But what about the complexity of derivatives? How does an executive with little or no experience in derivatives educate the board and equip his/her team? How will swaps be managed? The majority of banks choose to partner with an independent third party to do the heavy lifting of educating, equipping, and managing a customer swaps program. A good partner will serve as an advisor and advocate, ensuring that the bank is fully compliant and utilizing best practices.

Indirect swaps may be simple – but a traditional solution of offering swaps directly to borrowers is a better way to meet customer demand for long-term fixed-rate loans.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.