Naomi Snyder

Editor-in-Chief

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Editor-in-Chief Naomi Snyder is in charge of the editorial coverage at Bank Director. She oversees the magazine and the editorial team’s efforts on the Bank Director website, newsletter and special projects. She has more than two decades of experience in business journalism and spent 15 years as a newspaper reporter. She has a master’s degree in journalism from the University of Illinois and a bachelor’s degree from the University of Michigan.

Banking is not known for its innovative qualities, let’s face it. One could argue convincingly that the last great innovation in commercial banking was the ATM machine, first introduced in the United States in 1969. Many mobile banking apps leave something to be desired and checks take too long to process, while non-bank competitors such as PayPal and Wal-Mart Stores Inc. are gobbling up market share for everything from payments to loans.

Banking is not known for its innovative qualities, let’s face it. One could argue convincingly that the last great innovation in commercial banking was the ATM machine, first introduced in the United States in 1969. Many mobile banking apps leave something to be desired and checks take too long to process, while non-bank competitors such as PayPal and Wal-Mart Stores Inc. are gobbling up market share for everything from payments to loans.

Commercial banking—I’m not talking about the wild ride of investment banking—is conservative for good reason. Banks have long enjoyed special status as the safe house for everybody’s money, not to mention the source of a great deal of the economy’s funding—status that has led to heavy regulation to protect that system. That conservative bone inside the body of nearly every commercial banker leads to a reluctance to spend unnecessarily on technology, or waste shareholder investment, as well as skepticism toward new-fangled products.

But technology has an important role to play in attracting and retaining customers. Boards and management teams should not sit around and watch their customers go elsewhere as the competition installs new technology and steals market share. In an age where customers are increasingly comfortable with mobile banking applications, or shopping online for auto or home loans, your bank will need to pay attention to trends. It is possible to lose customers because you assumed the old way was the best way. Do you really think people under the age of 40 are going to real estate agents to get referrals to mortgage lenders? Or are they going to Yelp, or Angie’s List or Facebook? Some community bankers have expressed a fear to me that their banks might soon become irrelevant.

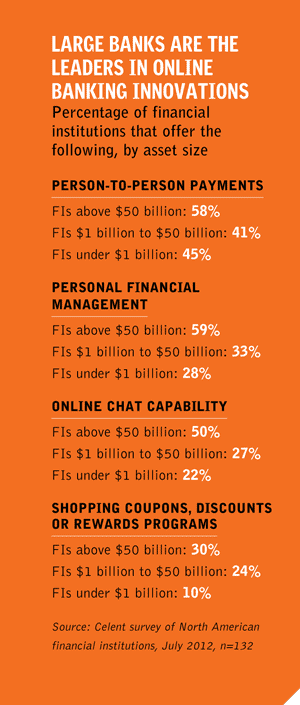

Bank boards clearly have to define their bank’s strategy as it relates to technology. There is no need to be an early adopter if you don’t want to be. The biggest banks use technology to enhance customer service and improve the bottom line, including person-to-person payments and online chat, but smaller banks are definitely finding these technologies useful as well. Banks well below the $50-billion asset mark offer coupons with mobile banking, mobile picture pay and personal financial management tools. “If you are a community bank, it’s unlikely that you are going to have a world leading platform,’’ says The Boston Consulting Group’s Corey Booth. “You don’t have the resources. You might want to keep up with the Jones’ or whatever Fiserv gives you. You have to decide your posture.”

All of this makes writing a special section on innovation in banking a challenging task. We wanted to show ways that new technology or innovative ideas really were changing the game for some banks in terms of retaining customers, increasing market share or improving efficiencies and profits. We looked for innovations, not necessarily technological ones, that made a measurable improvement. Of course, mobile banking is clearly changing the way banks deliver services. More transactions are conducted remotely than ever before, and branch traffic is dwindling. Everyone knows that. But what new mobile applications make some banks stand out in terms of ease of use and efficiencies? For some banks, mobile photo bill pay is attracting new customers. Personal financial management tools hold the promise of generating fee income. How are some banks achieving efficiencies with innovative branch designs that allow for a combination of self-service and a personal touch? At Extraco Banks in Temple, Texas, for example, image-enabled ATMs are handling about 20 percent of the $1.2-billion asset bank’s deposits. Data analytics is another innovation that banks are increasingly using to effectively target marketing campaigns. Minneapolis-based U.S. Bancorp, for example, tracks customers’ online behavior and transactions, so the bank can send personalized messages or even call them on the phone when the data “flags” them as good sales prospects. The data analysis is so sophisticated that the bank can prioritize prospects based on the likelihood of closing a sale and adjust the delivery message based on that. And finally, voice biometrics at Barclays is quickly handling security so customers don’t get bogged down in a call center “miserable moment”. And the customers love it.

All of this makes writing a special section on innovation in banking a challenging task. We wanted to show ways that new technology or innovative ideas really were changing the game for some banks in terms of retaining customers, increasing market share or improving efficiencies and profits. We looked for innovations, not necessarily technological ones, that made a measurable improvement. Of course, mobile banking is clearly changing the way banks deliver services. More transactions are conducted remotely than ever before, and branch traffic is dwindling. Everyone knows that. But what new mobile applications make some banks stand out in terms of ease of use and efficiencies? For some banks, mobile photo bill pay is attracting new customers. Personal financial management tools hold the promise of generating fee income. How are some banks achieving efficiencies with innovative branch designs that allow for a combination of self-service and a personal touch? At Extraco Banks in Temple, Texas, for example, image-enabled ATMs are handling about 20 percent of the $1.2-billion asset bank’s deposits. Data analytics is another innovation that banks are increasingly using to effectively target marketing campaigns. Minneapolis-based U.S. Bancorp, for example, tracks customers’ online behavior and transactions, so the bank can send personalized messages or even call them on the phone when the data “flags” them as good sales prospects. The data analysis is so sophisticated that the bank can prioritize prospects based on the likelihood of closing a sale and adjust the delivery message based on that. And finally, voice biometrics at Barclays is quickly handling security so customers don’t get bogged down in a call center “miserable moment”. And the customers love it.

While it may be a few more years before we see anything revolutionize the efficient delivery of services across the board like the ATM did in 1969, we can at least take a look at truly innovative designs and solutions that are changing the experience for some banks, and for their customers. We hoped to find those nuggets of change that are making a real difference.

Editor-in-Chief Naomi Snyder is in charge of the editorial coverage at Bank Director. She oversees the magazine and the editorial team’s efforts on the Bank Director website, newsletter and special projects. She has more than two decades of experience in business journalism and spent 15 years as a newspaper reporter. She has a master’s degree in journalism from the University of Illinois and a bachelor’s degree from the University of Michigan.