Kiah Lau Haslett

Banking & Fintech Editor

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Kiah Lau Haslett is the Banking & Fintech Editor for Bank Director. Kiah is responsible for editing web content and works with other members of the editorial team to produce articles featured online and published in the magazine. Her areas of focus include bank accounting policy, operations, strategy, and trends in mergers and acquisitions.

Are rising rates good for banks, or bad for them?

One way banks can answer that question- and position themselves to benefit from rising rates – is by measuring and managing their interest rate risk, or IRR. One way banks can calculate their long-term interest rate risk is using an economic value of equity, or EVE, model, which can show how interest rate movements will change the fair, or market, value of its assets, liabilities and equity. But rising deposit costs and changing depositor behavior is complicating those calculations.

“Economic value of equity (EVE) measurements allow for longer-term earnings and capital analysis. The analysis may be useful for long-term planning and may also indicate a need for short-term actions to mitigate IRR exposure,” the Federal Deposit Insurance Corp. wrote in its examination manual.

EVE is the difference between a bank’s asset cash flows and the liability cash flows, which includes deposits, says Matthew Tevis, a managing partner at Chatham Financial. This figure differs from a bank’s total equity because EVE includes the franchise value of deposits; bank deposits become more valuable as rates rise because they’re usually stable and less sensitive to price. But how a bank should model deposit costs and runoff – especially as rates rise – are the biggest unknowns in EVE calculations, Tevis says. In contrast, it’s easier for banks to calculate the market value of assets.

“The real challenge [with EVE] is on the liability side, because you have to assume that a certain amount of your deposit is going to be there for a period of time,” he says.

Tevis helps banks perform rate modeling exercises so they can see how their EVE changes with different interest rate movements – for example, rates rising by 200 basis points or falling 100 basis points. These exercises can show where the bank is carrying risk that could exceed its predetermined IRR policy limits.

Poor interest rate risk management played a large role in the March failure of Santa Clara, California-based Silicon Valley Bank, according to the Federal Reserve’s postmortem report. The April report found that the bank’s management “ignored potential longer-term negative impacts to earnings highlighted by the EVE metric.”

Silicon Valley reported in its 2021 annual report that its EVE was $20.7 billion, which was $4.1 billion above its total equity, but that EVE would fall sharply if rates jumped, The Wall Street Journal reported in May. The bank did not include EVE in its 2022 annual report, which was filed weeks before its March failure.

The Fed found that Silicon Valley’s risk appetite statement, set by the board, only included net interest income metrics and not EVE. But the bank did calculate EVE, and breached it multiple times before failure. Instead of addressing the underlying risks generating these breaches, management changed assumptions, like the duration of its deposits.

“No risk had been taken off the balance sheet,” the Fed wrote. “The assumptions were unsubstantiated given recent deposit growth, lack of historical data, rapid increases in rates that shorten deposit duration, and the uniqueness of [the bank’s] client base.”

The report goes onto say that the full board should understand and regularly review IRR reports that detail the level and trend of a bank’s exposure.

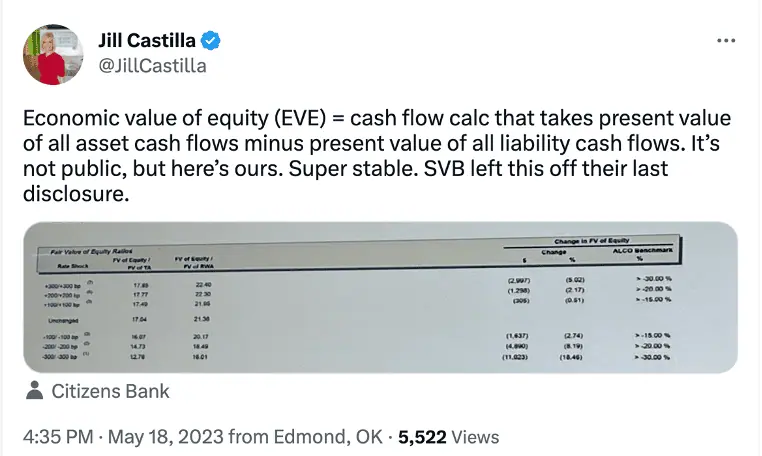

The board of Citizens Bank of Edmond discusses EVE during the monthly asset/liability committee meetings, says CEO Jill Castilla, who shared the privately held bank’s modeling on her Twitter feed recently. The spring banking crisis was an opportunity for the $388.5 million bank, based in Edmond, Oklahoma, to revisit and potentially update its EVE assumptions. The bank commissions deposit studies periodically to analyze how funding behaved in different rate environments and economic cycles, to bolster the credibility of its liability assumptions. Castilla adds that the committee invites input from two separate third-party experts and back-tests its ALCO model to see how closely bank performance mirrored what they modeled.

“It’s important for boards to be asking for deposit studies,” she says. “These are conducted by a third party and they’re able to feed into the assumptions in the model and the disclosure of any changes within the model … We’re questioning if our assumptions are still valid and correct and we’re making some adjustments based upon what we think, but it’s important as a management team to have studies to validate those observations.”

There are two common ways banks can address interest rate risk: changing the actual assets and liabilities, or laying hedges on top of the balance sheet inputs that counteract the impact of interest rates.

Banks are concerned that rates are going to continue rising, Tevis says: 75% of Chatham’s hedging work for banks right now is directed toward mitigating the risk from rising rates.

Ultimately, EVE isn’t a perfect mirror of bank interest rate risk: It’s an internal calculation done by the bank that is full of assumptions. Its outputs are only as accurate as its inputs. And while bank EVE may be stressed in the high interest rate environment, the Federal Open Market Committee’s pausing rate increases, or even potentially lowering rates, could shift the calculations and assumptions that go into the model or the result itself.

“When you’re doing an EVE analysis, you’re modeling both increases and decreases and you’re protecting yourself in either environment,” Castilla says. “As managers of banks, we’re also supposed to be expert risk managers and that includes interest rate risk. We have to protect ourselves on the upside and the downside.”

Risk issues like these will be covered during Bank Director’s Bank Audit & Risk Conference in Chicago June 12-14, 2023.

Kiah Lau Haslett is the Banking & Fintech Editor for Bank Director. Kiah is responsible for editing web content and works with other members of the editorial team to produce articles featured online and published in the magazine. Her areas of focus include bank accounting policy, operations, strategy, and trends in mergers and acquisitions.