Paul Mackowick

Getting your Digital Growth Strategy Right from the Start

Brought to you by Alpharank

Digital growth is only as good as the metrics used to measure it.

Growth is one of an executives’ most important responsibilities, whether that comes from the branch, through mergers and acquisitions or digital channels. Digital growth can be a scalable and predictable way for a bank to grow, if executives can effectively and accurately measure and execute their efforts. By using Net Present Value as the lens to evaluate digital marketing, a bank’s leadership team can make informed decisions on the future of the organization.

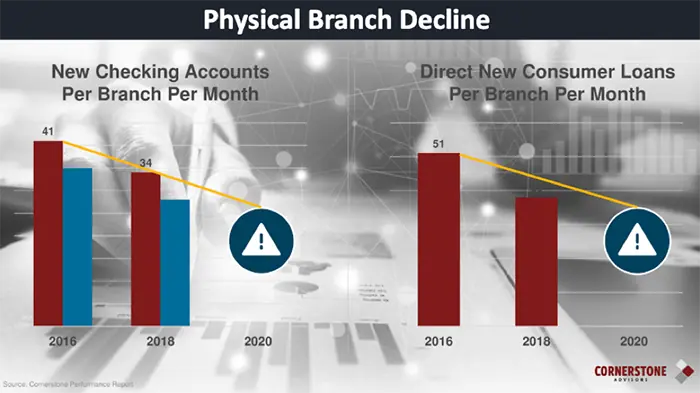

Banks need a well-thought-out digital growth strategy because of the changing role of the branch and big bank competition. The branch used to spearhead an institution’s growth efforts, but that is changing as branch sales decline. At the same time, the three biggest banks in the country rang up 50% of the new deposit account openings last year (even though they have only 24% of branches) as they lure depositors away from community banks, given regulators’ prohibition on acquisition.

Image courtesy of Ron Shevlin of Cornerstone Advisors

Image courtesy of Ron Shevlin of Cornerstone Advisors

Even in the face of these changes, many institutions are nervous about adopting an aggressive digital growth plan or falter in their execution.

A typical bank’s digital marketing efforts frequently rely on analytics that have been designed for another business altogether. They may want to place a series of ads on digital channels or social media sites, but how will they know if those work? They may use data points such as clicks or views to gauge the effectiveness of a campaign, even if those metrics don’t speak to the conversion process. They will also track metrics such as the number of new accounts opened after the start of a campaign or relate the number of clicks placed in new accounts.

But this approach assumes a direct link between the campaign and the new customers. In addition, acquisition and data teams will spend valuable time creating reports from disparate data sources to get the proper measurement, instead of analyzing generated reports to come up with better strategies.

Additionally, a bank’s CFO can’t really measure the effectiveness of an acquisition campaign if they aren’t able to see how the relationships with these new customers flourish and provides value to the institution. The conversion is not over with a click — it’s continuous.

This leads to another obstacle to measuring digital growth efforts: communication. Banks use three internal teams to generate growth: finance to fund the efforts; marketing to execute and measure it; and operations to provide the workflow to fulfill it.

Each team measures and expresses success differently, and each has its inherent shortcomings. Finance would like to know the cost and profitability of the new deposits generated, to assess the efficiency of the spend. Marketing might consider clicks or views. Operations will report on the number of accounts opened, but do not know definitively if existing workflows support the market segmentation that the bank seeks.

There is not a single group of metrics shared by the teams. However, the CEO will be most interested in cost of acquisition, the long-term profitability of the accounts and the return on investment of the total efforts.

But it’s now possible for banks to see the full measurement of their digital campaigns, from the disbursement of funds provided by the finance group to the success of these campaigns, in terms of deposits raised and net present value generated. These ads entice prospects into the account origination funnel, managed by operations, who open accounts and deposit initial funds. Those new customers then go through an onboarding process to switch their direct deposits and bill pay accounts. The new customer’s engagement can be measured six to 12 months later for value, and tied back to the original investment that brought them in the first place.

Bank leadership needs to be able to make decisions for the long-term health of their organizations. CEOs tell us they have a “data problem” when it comes to empowering their decisions. For this to work, the core system, the account origination funnel and the marketing channels all need to be tied together. This is true Integrated Value Measurement.