Niki Nolan

Senior Consultant

Enter your email address and password below to gain access.

To login to the Online Training Series, please click here.

Boards should address incentive plan risk mitigation, controls and governance processes ahead of the finalization of Section 956.

Niki Nolan is a senior consultant at Meridian Compensation Partners, LLC. She joined Meridian as an intern in the summer of 2014 and began as a consultant in 2015. She consults on a wide range of executive compensation matters, including executive and outside director compensation benchmarking, peer group development, short- and long-term incentive design, pay and performance analyses, and realizable/realized pay assessments.

Ms. Nolan has worked with a broad range of industries including retail, business services, and has also worked with public, private and non-profit companies. She is a member of Meridian’s financial services team. Additionally, Ms. Nolan is involved in research relating to governance and design, compensation trends, severance plan design, and relative TSR plans.

Dan is a Senior Consultant at Meridian Compensation Partners with experience advising compensation committees and senior management on a range of executive compensation matters and other human capital related issues.

When Silicon Valley Bank failed earlier this year, followed in quick succession by Signature Bank and First Republic Bank, regulators faced tough questions about their effectiveness and their actions to prevent such failures. In response to these events, greater regulation and scrutiny of incentive plans seemed likely; in short order, the Securities and Exchange Commission added the finalization of Section 956 of the Dodd-Frank Act to its Regulatory Flexibility Agenda with a targeted date of April 2024.

Section 956 requires six regulatory bodies to work together to develop rules governing incentive compensation for banks with $1 billion in assets or more. Until the rules are finalized, banks should follow the existing regulatory guidance from the 2010 Interagency Guidance on Sound Incentive Compensation Practices. Now is a good time for boards to address incentive plan risk mitigation, controls and governance processes to ensure that one, your bank is in alignment with existing guidance, and two, that the compensation committee is prepared ahead of the finalization of Section 956.

Establishing a Controls-Oriented Process for Managing Risk in Incentive Plans

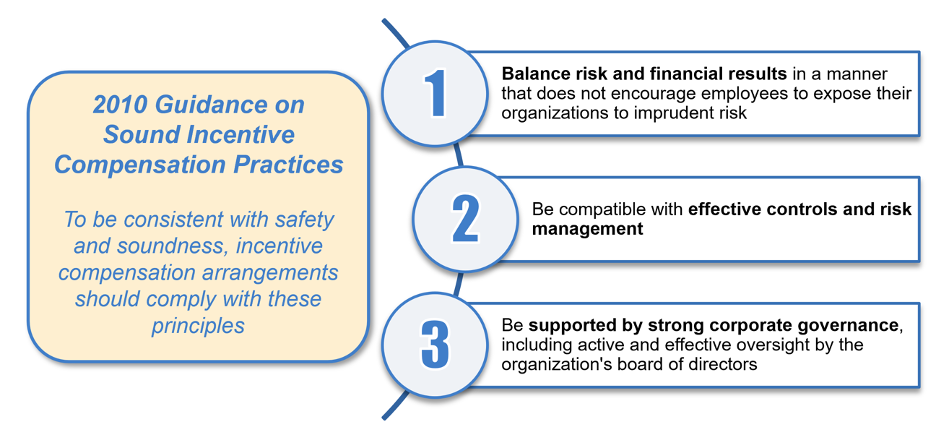

Boards are tasked with overseeing and reviewing executive incentive compensation programs and governance processes that align with the existing regulatory framework. However, they may soon be faced with more onerous incentive compensation requirements, rather than today’s principles-based guidance. The 2010 guidance establishes three principles that banks can review to prepare for greater regulation and enhance existing incentive compensation risk-related practices.

1. Balancing Risk and Financial Results

Under the 2010 Guidance, banks should design incentive compensation programs that consider risk against financial results. In response, banks have designed programs with the flexibility to reduce payouts for risk or compliance concerns, whether through a formulaic reduction or compensation committee discretion. Some incentive plans include mandatory deferrals, payouts in stock and/or reduced upside leverage. These features temper potential short-term gains, which may reduce the motivation for risky executive decision-making.

Many banks also implemented clawback policies in advance of the SEC’s mandatory policy, with triggers for inaccurate financial results, misconduct or significant risk management failures.

Beyond clawback policies, banks should consider the timing of payouts. Deferred payouts provide a mechanism for banks to reduce or forfeit incentives if significant risk concerns are identified. Many banks also use continued vesting upon termination or retirement, which may protect against short-term risky behavior in advance of an executive’s separation.

Before finalization of Section 956, compensation committees should ask:

2. Documentation, Effective Controls and Risk Management

Banks’ human resources, finance, risk and legal teams all have important roles in reviewing incentive plan risk. These teams should ensure there is a centralized process for reviewing and assessing risk before finalizing payouts.

Before finalization of Section 956, boards should review the bank’s incentive plan processes and controls and ask:

3. Strong Corporate Governance

The 2010 guidance provides clear regulatory expectations that compensation committees must provide strong oversight of incentive plans to ensure the programs do not encourage excessive risk.

Before finalization of Section 956, committees should consider the following:

While regulators are likely to continue focusing the most stringent rules on the largest U.S. banks, incentive compensation practices will trickle down to smaller regional and community banks. Incentive program design, controls and processes will undoubtedly change with the finalization of Section 956. Banks should ensure they are effectively adhering to existing regulatory guidance and be ready to respond once 956 rules are finalized.

Niki Nolan is a senior consultant at Meridian Compensation Partners, LLC. She joined Meridian as an intern in the summer of 2014 and began as a consultant in 2015. She consults on a wide range of executive compensation matters, including executive and outside director compensation benchmarking, peer group development, short- and long-term incentive design, pay and performance analyses, and realizable/realized pay assessments.

Ms. Nolan has worked with a broad range of industries including retail, business services, and has also worked with public, private and non-profit companies. She is a member of Meridian’s financial services team. Additionally, Ms. Nolan is involved in research relating to governance and design, compensation trends, severance plan design, and relative TSR plans.

Dan is a Senior Consultant at Meridian Compensation Partners with experience advising compensation committees and senior management on a range of executive compensation matters and other human capital related issues.