Nathan Stovall is the director of the financial institutions research team for S&P Global Market Intelligence, which is responsible for data-driven news and research focused on banks and insurers. Nathan has more than 20 years of experience covering the financial institutions sector, with a focus on U.S. banks.

He is the author of the banking blog, Street Talk, and host of the podcast by the same name. He publishes quarterly outlooks for the U.S. banking industry as well as a separate outlook focused exclusively on U.S. community banks.

Nathan Stovall

Director of FIG Research

SHARE THIS ARTICLE

Bankers maintain that their borrower base remains healthy, and the U.S. economy has proven resilient in the face of uncertainty created by protectionist trade policies, with job gains in June exceeding economists’ forecasts. However, credit quality continues to normalize as criticized loans are rising, while loan growth has fallen short of optimistic expectations early in the year.

Criticized loans at U.S. public banks rose again in the first quarter, with the median ratio of criticized loans to Tier 1 capital climbing to 20.04% from 18.52%. Banks classify loans as criticized if some sign of weakness emerges, but that migration does not necessarily suggest a future loss.

Much of the weakness and concern in the investment community relates to commercial real estate (CRE) loans. Some CRE borrowers face a double whammy of lower cash flows due to the rise of hybrid work and higher debt service stemming from increases in interest rates over the last few years. CRE delinquencies have risen for 10 consecutive quarters, but losses have often been less than many feared, in part due to well-funded distressed investors targeting the asset class. When banks have sold CRE loans — often in connection with an acquisition — sellers have recorded relatively modest discounts to par, ranging from 8% to 10%.

Consumer delinquencies have risen from historical lows as well. While many banks might not have sizable consumer or credit card portfolios, the consumer drives the economy. A weakened consumer could push the U.S. into a recession. Currently, the American consumer is stretched — savings rates have slowed, and excess savings accumulated during the pandemic have been exhausted — but fortunately, the consumer is not yet broken.

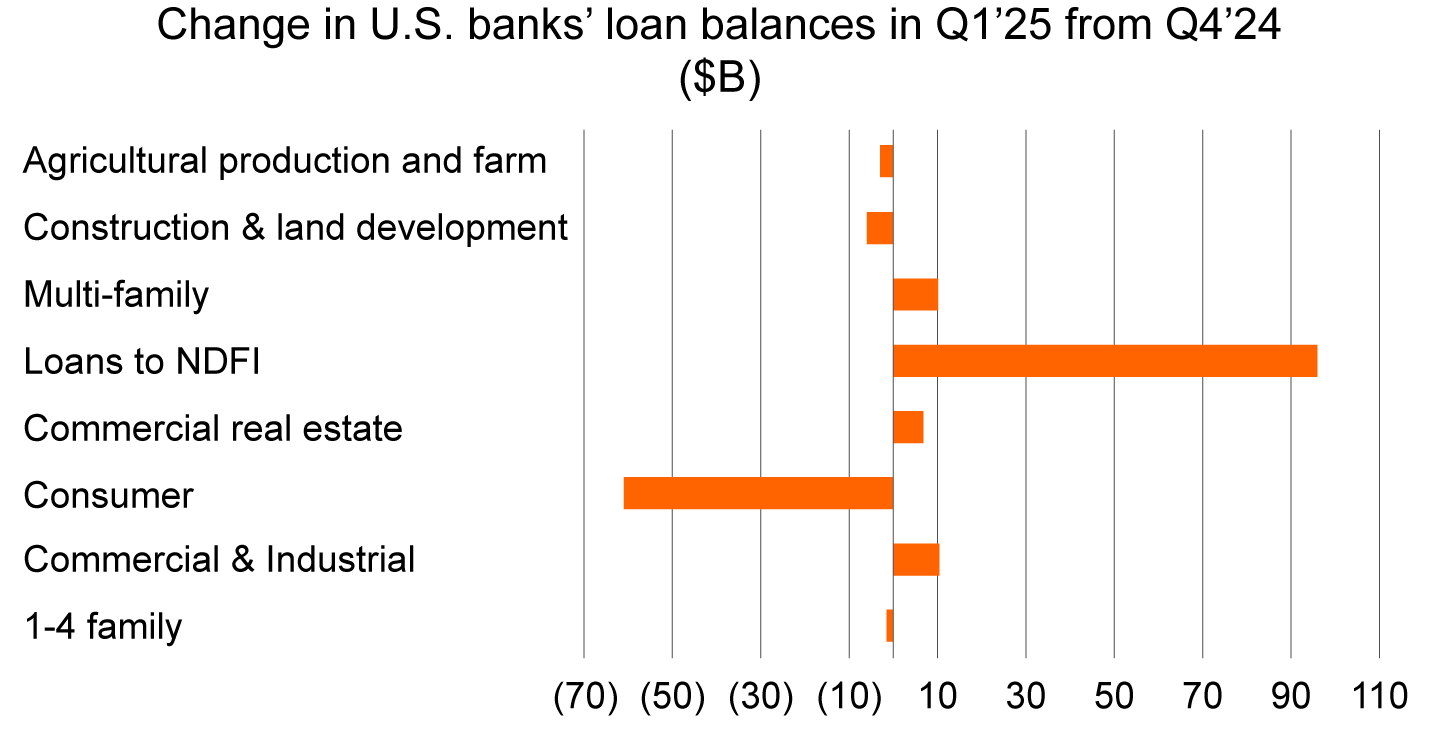

Loan growth has been a bigger disappointment, falling short of expectations that pro-growth policies and deregulation from the Trump administration would spur increased borrower demand. Uncertainty from tariffs that surfaced early in the second quarter seems to have weighed on borrowers’ expansion plans. The Federal Reserve Board’s H.8 data shows that loans have grown 2.75% through the first half of the year, with stronger growth occurring in the first quarter. Notably, loans to non-depository financial institutions, including private credit firms that compete with banks, were by far the biggest driver of growth in the first quarter.

Bankers likely will find that strong loan growth will be tough to come by, and it could be prudent to avoid pressuring lenders aggressively at this point in the cycle. Competition should remain fierce as credit is widely available to corporate borrowers through the high-yield, leveraged loan and competing private credit markets. Credit spreads widened when tariffs first surfaced in early April but have since tightened back near record levels.

Rather than fighting to meet their organic growth goals, bank managers should move in the other direction and encourage lenders to tighten pricing and lending standards, increase debt service coverage ratios and move away from their least creditworthy borrowers.

While lower loan volumes may reduce earnings in the near term, avoiding risk today could pay dividends further down the road and help banks minimize credit losses. The approach could also help institutions to improve their funding bases, which represent the true value of a banking franchise. Slower loan growth would reduce a bank’s funding need and allow for quicker reductions in deposit costs. Banks are already benefitting from the remixing of their balance sheets as higher-cost certificate of deposits (CDs) roll off their books, but the pace of improvement could be even more pronounced.

A stronger funding base and continued strength in credit quality would be rewarded by investors and appeal to potential acquirers. Banks that are willing to take step back and operate more cautiously now will also have a greater opportunity to continue growing, both organically and through acquisitions, when the next downturn occurs.

WRITTEN BY

Nathan Stovall

Director of FIG Research

Nathan Stovall is the director of the financial institutions research team for S&P Global Market Intelligence, which is responsible for data-driven news and research focused on banks and insurers. Nathan has more than 20 years of experience covering the financial institutions sector, with a focus on U.S. banks.

He is the author of the banking blog, Street Talk, and host of the podcast by the same name. He publishes quarterly outlooks for the U.S. banking industry as well as a separate outlook focused exclusively on U.S. community banks.