David Sweeney

Managing Director

Enter your email address and password below to gain access.

Dave Sweeney is a managing director at Chatham Financial. Mr. Sweeney leads the business development efforts in the Midwest where he advises financial institutions on hedging strategies. He runs the investment and treasury advisors team.

Prior to joining Chatham Financial, Mr. Sweeney spent 14 years with Ernst & Young as a principal in the financial institutions practice, and served as treasurer and chief investment officer for two community banks. Mr. Sweeney has experience marketing and selling interest rate derivative products to commercial bank loan customers.

After eight years of waiting for interest rates to make a meaningful move higher, the fed funds rate is making a slow creep towards 2 percent. With a more volatile yield curve expected in the upcoming years and continued competition for loans, net interest margins (NIM) may continue to compress for many financial institutions. The key to achieve NIM expansion will involve strong loan pricing discipline and the full toolkit of financial products to harvest every available basis point.

After eight years of waiting for interest rates to make a meaningful move higher, the fed funds rate is making a slow creep towards 2 percent. With a more volatile yield curve expected in the upcoming years and continued competition for loans, net interest margins (NIM) may continue to compress for many financial institutions. The key to achieve NIM expansion will involve strong loan pricing discipline and the full toolkit of financial products to harvest every available basis point.

Where to look on the balance sheet? Here are some suggestions.

Loan Portfolio

The loan portfolio is a great place to look for opportunities to improve the profitability. Being able to win loans and thus grow earning assets is critical to long-term success. A common problem, however, is the mismatch between market demand for long-term, fixed rate loans and the institution’s reluctance to offer the same.

Oftentimes, a financial institution’s interest rate risk position is not aligned to make long-term, fixed rate loans. A few alternatives are available to provide a win-win for the bank and the borrower:

With the ability to offer long-term fixed rate loans, the financial institution will open the door to greater loan volumes, improved NIM, and profitability.

How much does a financial institution leave on the table when prepayment penalties are waived? A common comment from lenders is that borrowers are rejecting prepayment language in the loan.

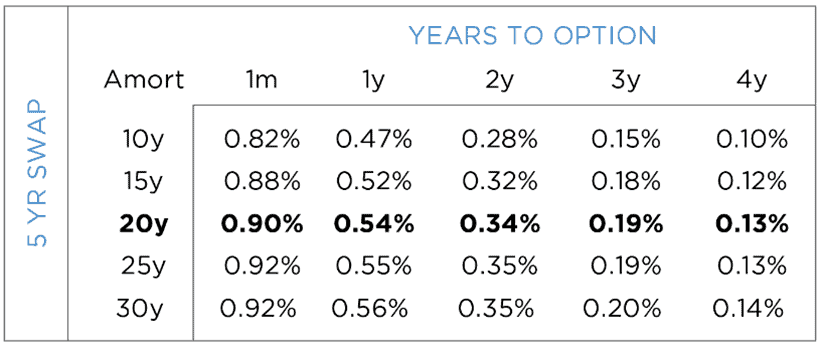

How much is this foregone prepayment language worth? As you can see from the table below, for a 5-year loan using a 20-year amortization, the value of not including prepayment language is 90 basis points per year.

At a minimum, financial institutions should look to write into the loan at least a 1- to 2-year lock out on prepayment, which drops the value of that option from 90 basis points to 54 basis points for a 1-year lock out or 34 basis points for a 2-year lock out. That may be more workable while staying competitive.

Investment Portfolio

The investment portfolio typically makes up 20 percent to 25 percent of earning assets for many institutions. Given its importance to the financial institution’s earnings, bond trade execution efficiency may be a way to pick up a basis point or two in NIM.

A financial institution investing in new issue bonds should look at the prospectus and determine the underwriting fees and sales concessions for the issuance. There are many examples in which the underwriting fees and sales concessions are 50 to 100 basis points higher between two bonds from the same issuer with the same characteristics, with both issued at par. To put that in yield terms, on a 5-year bond, the yield difference can be anywhere between 10 and 20 basis points per year.

If you are purchasing agency debentures in the secondary market, you can access all the information you need from the Financial Industry Regulatory Authority’s Trade Reporting and Compliance Engine (TRACE) to determine the mark up of the bonds you purchased. Using Bloomberg’s trade history function (TDH), in many cases, it is easy to determine where you bought the bond and how much the broker marked up the bond. Similar to the new issue example above, a mark-up of 25 to 50 basis points more than you could have transacted would equate to 5 to 10 basis points in yield on a 5-year bond.

For a typical investment portfolio, executing the more efficient transactions would increase NIM by 1.5 to 5 basis points. For many institutions, simply executing bond transactions more efficiently equates to a 1 percent to 3 percent improvement in return on assets and return on equity.

Wholesale Funding

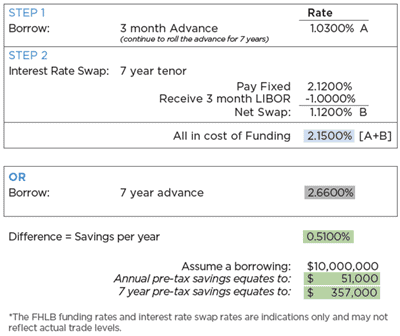

A financial institution can use short-term Federal Home Loan Bank (FHLB) advances combined with an interest rate swap to lock in the funding for the desired term. By entering into a swap coupled with borrowing short-term from the FHLB, an institution can save a significant amount of interest expense. Here is an example below:

Derivatives

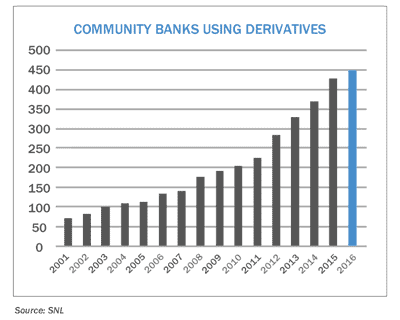

As you can see from a few of the previous examples, derivatives can be useful tools. Getting established to use derivatives takes some time, but once in place, management will have a tool that can quickly be used to take advantage of inefficient market pricing or to change the interest rate risk profile of the institution.

Number of Community Banks Using Derivatives, by Year

Conclusion

In a low interest-rate environment and with increased volatility in rates across the yield curve, net interest margins are projected to continue to be under pressure. The above suggestions could be crucial to ensuring long-term success. Offering longer-term loans and instilling more efficient loan pricing is the start to improved financial performance.

Dave Sweeney is a managing director at Chatham Financial. Mr. Sweeney leads the business development efforts in the Midwest where he advises financial institutions on hedging strategies. He runs the investment and treasury advisors team.

Prior to joining Chatham Financial, Mr. Sweeney spent 14 years with Ernst & Young as a principal in the financial institutions practice, and served as treasurer and chief investment officer for two community banks. Mr. Sweeney has experience marketing and selling interest rate derivative products to commercial bank loan customers.