Brandon Koeser

Director, Risk Consulting

Enter your email address and password below to gain access.

Brandon Koeser is a senior manager of assurance services at RSM US LLP. He is an analyst in RSM’s cutting-edge Industry Eminence Program, positioning him to understand, forecast and communicate economic, business and technology trends shaping the industries RSM serves. His focus is on advising financial institutions and capital markets leaders and clients on business conditions, industry trends and regulatory developments influencing their ecosystems across North America.

Mr. Koeser has over 15 years of experience serving clients across the country by providing industry-specific insights and thought leadership that allows them to stay at the forefront of the changes within their industry while also providing assurance and risk advisory services, including financial statement audits, attest engagement services, operational risk assessments and specialized compliance audits.

It’s a perfect storm for bank directors and their institutions: Increasing credit risk, low interest rates and the corrosive effects of the coronavirus culminating into a squeeze on their margins.

The pressure on margins comes at the same time as directors contend with a fundamental new reality: Traditional banking, as we know it, is changing. These changes, and the speed at which they occur, mean directors are wrestling with the urgent task of helping their organizations adapt to a changing environment, or risk being left behind.

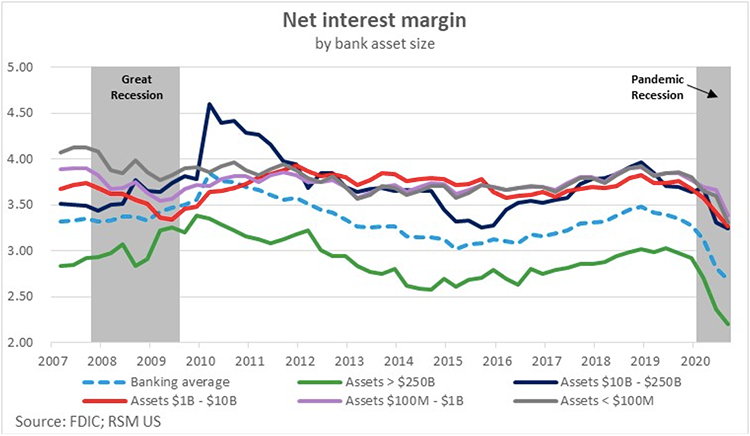

As books close on 2020 with a still-uncertain outlook, the most recent release of the Federal Deposit Insurance Corp.’s Quarterly Banking Profile underlines the substantial impact of low rates. For the second straight quarter, the average net interest margin at the nation’s banks dropped to its lowest reported level.

The data shows that larger financial institutions have felt the pain brought about by this low-rate environment first. But as those in the industry know, it is often only a matter of time until smaller institutions feel the more-profound effects of the margin contraction. The Federal Reserve, after all, has said it will likely hold rates at their current levels through 2023.

In normal times, banks would respond to such challenges by cutting expenses. But these are not normal times: Such strategies will simply not provide the same long-term economic benefits. The answer lies in technology. Making strategic investments throughout an organization can streamline operations, improve margins and give customers what they want.

Survey data bears this out. Throughout the pandemic, J.D. Power has asked consumers how they plan to act when the crisis subsides. When asked in April about how in-person interactions would look with a bank or financial services provider once the crisis was over, 46% of respondents said they would go back to pre-coronavirus behaviors. But only 36% of respondents indicated that they would go back to pre-Covid behaviors when asked the same question in September. Consumers are becoming much more likely to use digital channels, like online or mobile banking.

These responses should not come as a surprise. The longer consumers and businesses live and operate in this environment, the more likely their behaviors will change, and how banks will need to interact with them.

Bank directors need to assess how their organizations will balance profitability with long-term investments to ensure that the persistent low-rate environment doesn’t become a drag on revenue that creates a more-difficult operating situation in the future.

The path forward may be long and difficult, but one thing is certain: Banks that aren’t evaluating digital and innovative options will fall behind. Here are three key areas that we’ve identified as areas of focus.

While we do not expect branch banking to disappear, we do expect it to change. And while all three technology investment alternatives are reasonable options for banks to adapt and survive in tomorrow’s next normal, it is important to know that failing to appropriately invest will lead to challenges that may be far greater than what are being experienced today.

Brandon Koeser is a senior manager of assurance services at RSM US LLP. He is an analyst in RSM’s cutting-edge Industry Eminence Program, positioning him to understand, forecast and communicate economic, business and technology trends shaping the industries RSM serves. His focus is on advising financial institutions and capital markets leaders and clients on business conditions, industry trends and regulatory developments influencing their ecosystems across North America.

Mr. Koeser has over 15 years of experience serving clients across the country by providing industry-specific insights and thought leadership that allows them to stay at the forefront of the changes within their industry while also providing assurance and risk advisory services, including financial statement audits, attest engagement services, operational risk assessments and specialized compliance audits.