Ben Lewis

Managing Director and Global Head of Sales

Enter your email address and password below to gain access.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.

Financial markets have been rocked by significant volatility in 2022.

Over the first six months of 2022, the 10-year U.S. Treasury rate jumped from 1.52% to 3.2%. A confluence of events is driving that volatility: increased inflation expectations led to more significant and sooner-than-expected increases in the Federal Funds rate, uncertainty of the first military conflict in Europe since World War II, and the economy. Financial institutions are finding themselves in very turbulent waters.

Banks that prepared for this possibility are navigating across these choppy waters with greater ease. They’re using prudent risk management tools, like interest rate swaps, to smooth earnings and protect against continued increases in long-term rates. Swaps create more flexibility for banks: they can be quickly and easily implemented and allow institutions to bifurcate the rate risk from traditional assets and liabilities.

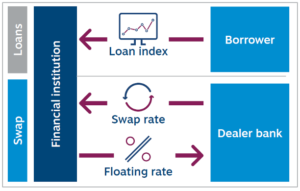

Most banks use hedging strategies that aim to smooth earnings. For example, banks use an interest rate swap to convert a portion of their floating-rate assets to fixed. They lock in the market’s expectations for rates and bring forward future expected income.

The benefits of this strategy:

When it comes to hedging floating rate loans, we see a mix of Fed Funds (to hedge loans tied to Prime), SOFR, LIBOR, and a handful of banks using that Bloomberg Short-Term Bank Yield (BSBY) index.u202f Additionally, hedging floating rate loans with floors requires special considerations.

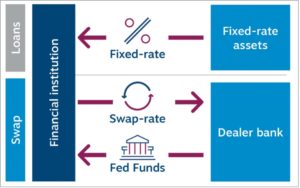

On the other side of the spectrum, those banks hedging for rising rates primarily use swap and cap strategies to reduce duration risk in the loan and bond portfolio. Notably, the Financial Accounting Standards Board recently introduced the portfolio layer method, which allows banks to swap pools of fixed-rate assets like loans or securities to floating.

The benefits of this strategy:

In the turbulent seas of this current moment, banks prepared to use hedging strategies enjoy the benefits of smoother income and mitigated rate volatility. They also benefit from their flexibility: Banks can quickly execute swaps, allowing it to bifurcate the rate risk from traditional assets and liabilities. Finally, derivatives have low capital requirements, resulting in minimal impact to capital ratios.

Adding hedging tools to the tool kit now allows your bank to get ready before next quarter’s volatility – and potential rate change – is best practice that can be accomplished quickly and efficiently.

Ben Lewis is a managing director and global head of sales for Chatham’s Financial institutions practice. Mr. Lewis has worked with depositories of all sizes helping them manage interest rate risk through the prudent use of hedging strategies. Prior to his work with financial institutions, Mr. Lewis worked with private equity firms and REITs to hedge their interest rate and foreign currency risk.

Prior to joining Chatham, Mr. Lewis served 8 years in the U.S. Navy as a P-3C Orion Naval flight officer serving in both Operation Enduring Freedom and Operation Iraqi Freedom.