John Maxfield

Freelancer

Enter your email address and password below to gain access.

John Maxfield is a freelance writer for Bank Director magazine. He was previously the senior banking specialist at The Motley Fool. He regularly writes for Bank Director magazine and BankDirector.com. His work has been syndicated widely to national publications including USA Today, Time and Business Insider, and he’s been a regular guest on CNBC. John has a bachelor’s degree in economics from Lewis & Clark College and a juris doctorate from Southern Methodist University. He’s a licensed attorney in the State of Oregon.

One thing that separates great bankers from their peers is a deep appreciation for the highly cyclical nature of the banking industry.

One thing that separates great bankers from their peers is a deep appreciation for the highly cyclical nature of the banking industry.

Every industry is cyclical, of course, thanks to the cyclical nature of the economy. Good times are followed by bad times, which are followed by good times. It’s always been that way, and there’s no reason to think it will change anytime soon.

Yet, banking is different.

The typical bank borrows $10 for every $1 in equity. On one hand, this leverage accelerates the economic growth of the communities a bank serves. But on the other, it makes banks uniquely sensitive to fluctuations in employment and asset prices.

Even a modest correction in the business cycle or a major asset class can send dozens of banks into receivership.

“It is in the nature of an industry whose structure is competitive and whose conduct is driven by supply to have cycles that only end badly,” wrote Barbara Stewart in “How Will This Underwriting Cycle End?,” a widely cited paper published in 1980 on the history of underwriting cycles.

Stewart was referring to the insurance industry, but her point is equally true in banking.

This is why bankers with a big-picture perspective have an advantage over bankers without a similarly deep and broad appreciation for the history of banking, combined with knowledge about the strengths and infirmities innate in a bank’s business model.

How does one go about gaining a big-picture perspective?

You can do it the hard way, by amassing personal experience. If you’ve seen enough cycles, then you know, as Jamie Dimon, the CEO of JPMorgan Chase & Co., has said: “You don’t run a business hoping you don’t have a recession.”

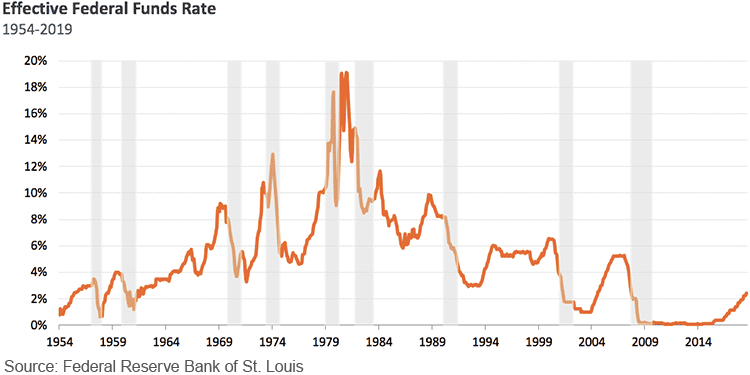

Or you can do it the easy way, by accruing experience by proxy—that is, by learning how things unfolded in the past. If you know that nine out of the last nine recessions were all precipitated by rising interest rates, for instance, then you’re likely to be more cautious with your loan portfolio in a rising rate environment.

You can see this in the chart below, sourced from the Federal Reserve Bank of St. Louis’ popular FRED database. The graph traces the effective federal funds rate since 1954, with the vertical shaded portions representing recessions.

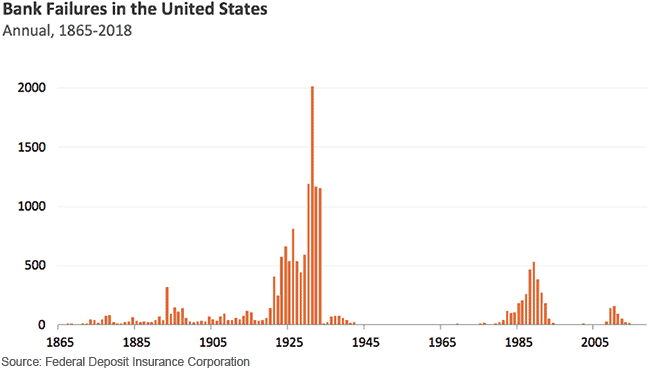

A second chart offering additional perspective on the cyclical nature of banking traces bank failures since the Civil War, when the modern American banking industry first took shape.

This might seem macabre—who wants to obsess over bank failures?—but this is an inseparable aspect of banking that is ignored at one’s peril. Good bankers respect and appreciate this, which is one reason their institutions avoid failure.

Not surprisingly, the incidence of bank failures closely tracks the business cycle. The big spike in the 1930s corresponds to the Great Depression. The spike in the 1980s and 1990s marks the savings and loan crisis. And the smaller recent surge corresponds to the financial crisis.

All told, a total of 17,365 banks have failed since 1865. A useful analog through which to think about banking, in other words, is that it’s a war of attrition, much like the conflict that spawned the modern American banking industry.

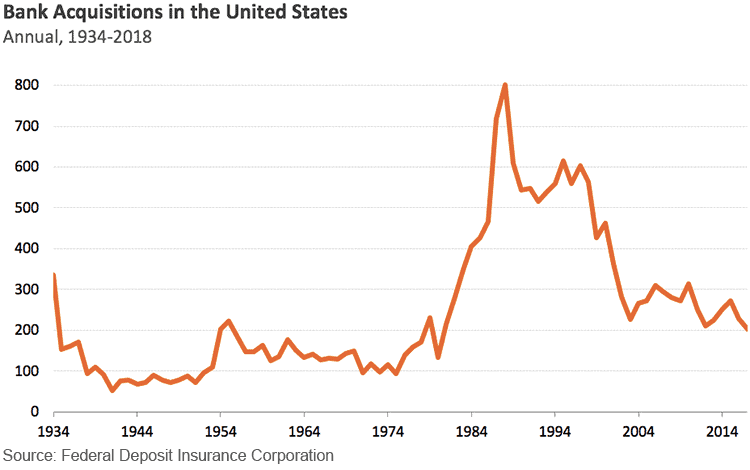

A third chart offering insight into how the banking industry has evolved in recent decades illustrates historical acquisition activity.

Approximately 4 percent of banks consolidate on an annual basis, equating to about 200 a year nowadays. But this is an average. The actual number has fluctuated widely over time. ![]()

From 1940 through the mid-1970s, when interstate and branch banking were prohibited in most states, there were closer to 100 bank acquisitions a year. But then, as these regulatory barriers came down in the 1980s and 1990s, deal activity surged.

The point being, while banking is a rapidly consolidating industry, the most recent pace of consolidation has decelerated. This is relevant to anyone who may be thinking of buying or selling a bank. It’s also relevant to banks that aren’t in the market to do a deal, as customer attrition in the wake of a competitors’ sale has often been a source of organic growth.

In short, it’s easy to dismiss history as a topic of interest only to professors and armchair historians. But the experience one gains by proxy from looking to the past can help bankers better position their institutions for the present and the future.

Take it from investor Charlie Munger: “There’s no better teacher than history in determining the future.”

John Maxfield is a freelance writer for Bank Director magazine. He was previously the senior banking specialist at The Motley Fool. He regularly writes for Bank Director magazine and BankDirector.com. His work has been syndicated widely to national publications including USA Today, Time and Business Insider, and he’s been a regular guest on CNBC. John has a bachelor’s degree in economics from Lewis & Clark College and a juris doctorate from Southern Methodist University. He’s a licensed attorney in the State of Oregon.