Bob Newman

Community Banks and Derivatives: Debunking the Four Biggest Myths

Brought to you by Chatham Financial

Close

About the authors

Written by

Bob Newman

Those of us who were in banking when Ronald Reagan entered the White House remember the interest rate rollercoaster ride brought about by the Federal Reserve when it aggressively tightened the money supply to tame inflation. It was during this era of unprecedented volatility that interest rate swaps, caps and floors were introduced to help financial institutions keep their books in balance. But over the years, opaque pricing, unnecessary complexity and misuse by speculators led Richard Syron, former chairman of the American Stock Exchange, to observe, “Derivative. That’s the 11-letter four-letter word.”

Those of us who were in banking when Ronald Reagan entered the White House remember the interest rate rollercoaster ride brought about by the Federal Reserve when it aggressively tightened the money supply to tame inflation. It was during this era of unprecedented volatility that interest rate swaps, caps and floors were introduced to help financial institutions keep their books in balance. But over the years, opaque pricing, unnecessary complexity and misuse by speculators led Richard Syron, former chairman of the American Stock Exchange, to observe, “Derivative. That’s the 11-letter four-letter word.”

As community banks bought into Syron’s “D-word” conclusion and resolved to avoid their use altogether, several providers fed these fears and designed programs that promise a derivative-free balance sheet. But many banks are beginning to question the effectiveness of these solutions.

Today, as commercial borrowers seek long-term, fixed-rate funding for 10 years and longer, risk-averse community banks want to know how to solve this term mismatch problem in a responsible and sustainable manner. The fact that Syron voiced his opinion on derivatives in 1995 suggests that now might be a good time to examine the roots of “derivative-phobia,” by considering what has changed in the past quarter-century and challenging four frequently heard biases against community banks using swaps.

1. None of my community bank peers use interest rate derivatives.

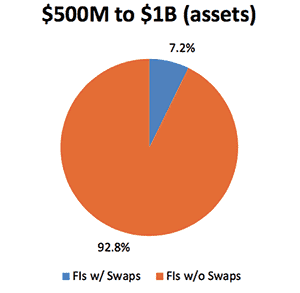

If you are not hedging with swaps, and your total assets are between $500 million and $1 billion, then you are in good company: More than nine out of ten of your peers have also avoided their use.

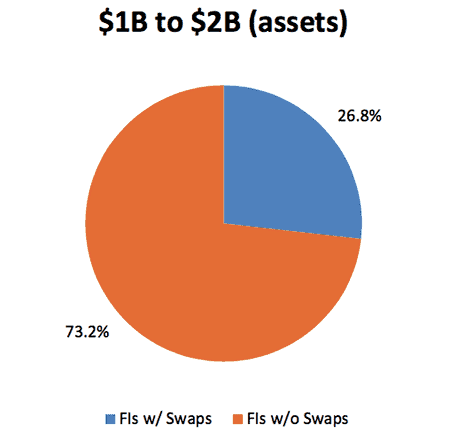

But if your bank is larger, or your growth plans anticipate crossing the $1 billion asset level, more than one in four of your new peers use swaps.

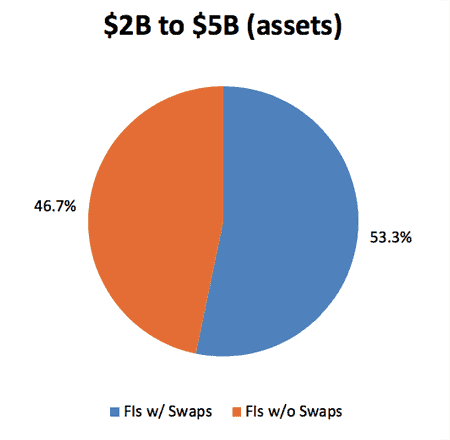

Once your bank crosses the $2 billion mark, more than half of your peers manage interest rate risk with derivatives, and institutions not using swaps become a shrinking minority.

Community banks should consider their growth path and the best practices of their expected peer group before dismissing out-of-hand the use of derivatives.

2. The derivatives market is a big casino, and swaps are always a bet.

While some firms (AIG in 2008, for example) have used complex derivatives to speculate, a vanilla swap designed to neutralize a bank’s natural risks operates as a hedge. Post-crisis, the Dodd-Frank Act brought more transparency to swap pricing, as swap dealers are now required to disclose the wholesale cost of the swap to their customers. In addition, most dealers are now willing to operate on a bilateral secured basis, removing most of the counterparty risk that the trading partners of Lehman Brothers experienced firsthand when that company collapsed. These changes in market practices have made it much more practical for community banks to execute simple hedging transactions at fair prices with manageable credit risk.

3. Derivatives accounting always results in unwanted surprises and volatility.

Derivatives missteps led to FAS 133—regarding the measurement of derivative instruments and hedging activities—being issued in 1998, bringing the fair value of derivatives out of the footnotes and onto the balance sheet for the first time. But the standard (now ASC 815) proved difficult to apply, leading to some notable financial restatements in the early 2000s. Fast forward nearly twenty years, and the Financial Accounting Standards Board has issued an overhaul to hedge accounting (ASU 2017-12) that is a game-changer for community banks. With mandatory adoption in 2019, there are more viable ways to solve the age-old mismatch facing banks. And the addition of fallback provisions, combined with improvements to “the shortcut method,” greatly reduces the risk of unexpected earnings volatility.

4. ISDA documents should always be avoided.

While admittedly lengthy, the Master Agreement published by the International Swaps and Derivatives Association was designed to protect both parties to a derivative contract and is the industry standard for properly documenting an interest rate swap. Many community banks seeking an ISDA-free solution for their customers are actually placing the borrower into a lightly-documented derivative with an unknown third-party. If a borrower is not sophisticated enough to read and sign the ISDA Master Agreement, they have no business executing a swap in the first place. A simpler solution is to make a fixed-rate loan and execute a swap behind the scenes to neutralize the interest rate risk. This keeps the swap and the agreement between two banks, and removes the borrower from the derivative altogether.

For community banks that have been trying to solve their mismatch problem in a manner that is derivative-free, it is worth re-examining the factors that have led to pursuing a derivatives-avoidance strategy, and counting the costs and hidden exposures involved in doing so.

WRITTEN BY