Sai Huda

The New FFIEC Information Security Examination Procedures: What Boards Should Be Doing Now

Close

About the authors

Written by

Sai Huda

How effective is your bank’s approach to information security, including cybersecurity? On September 9, the Federal Financial Institutions Examination Council (FFIEC) published new information security examination procedures. It is critical that boards and management teams quickly get up to speed on the new exam procedures so there are no surprises in the bank’s next exam that adversely impact earnings, capital or value creation.

How effective is your bank’s approach to information security, including cybersecurity? On September 9, the Federal Financial Institutions Examination Council (FFIEC) published new information security examination procedures. It is critical that boards and management teams quickly get up to speed on the new exam procedures so there are no surprises in the bank’s next exam that adversely impact earnings, capital or value creation.

The new exam procedures focus on assessing the quality and effectiveness of the bank’s information security program, including its culture, governance, security operations, with emphasis on cybersecurity, and assurance processes, such as self-assessments, penetration tests, vulnerability assessments and independent audits. The procedures contain eleven objectives for the examiners to attain.

The objective relating to security operations and cybersecurity is especially noteworthy, as it contains enhanced expectations. Both in the preamble and in the specific exam procedures, there is recognition that it is not a question of if, but when an attacker will break into the network, so banks need to enhance threat identification, monitoring, detection and response. Examiners will evaluate whether the bank has monitoring in place to identify malicious activity, a process to identify possible compromises in the bank’s systems, and whether it uses tools that reveal and trace an attacker’s actions, such as attack or event trees, to size up exposures and respond effectively.

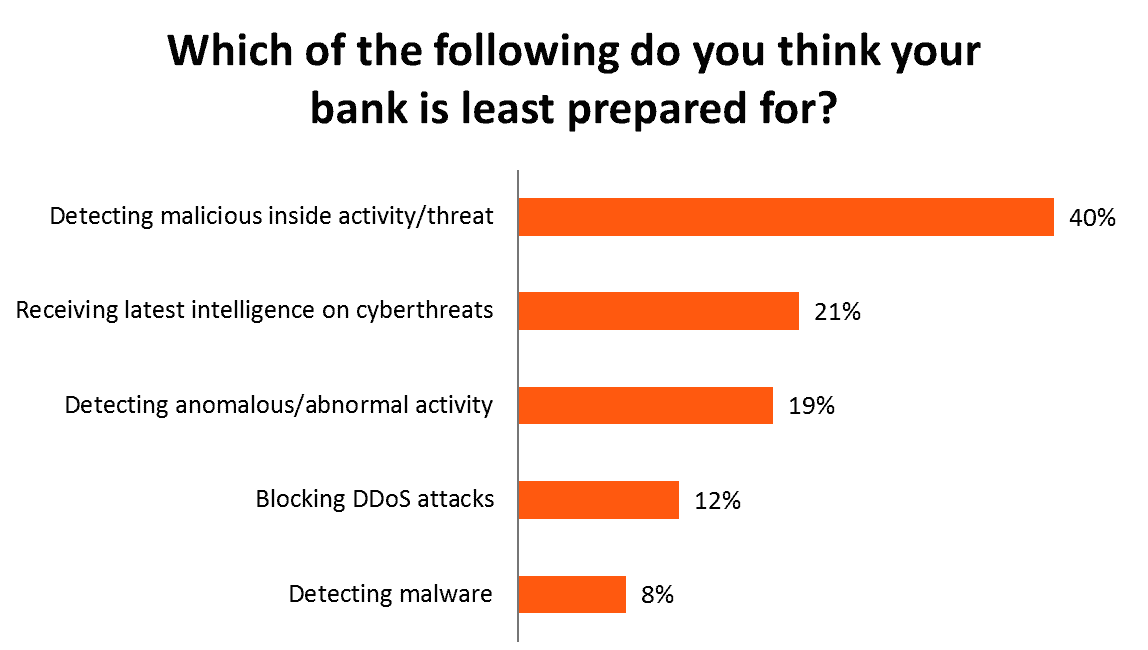

While speaking on cybersecurity on the main stage at Bank Director’s 2016 Bank Audit and Risk Committees Conference in June, I electronically polled the bank directors and senior executives in attendance. The results from the 206 respondents indicate a need for banks to beef up cybersecurity to meet these enhanced regulatory expectations. While cybersecurity is a top concern for bank boards, seventy-seven percent indicated that they do not review cybersecurity at every board meeting. Fifty-nine percent of attendees said that detecting anomalous activity or threats from malicious insiders are the cybersecurity risks for which their bank is least prepared.

Source: 206 respondents, Bank Director Audit and Risk Committees Conference June 2016

When I asked how many had implemented ongoing reviews of the network visibility map for risk oversight, only 31 percent had done so. This map visually shows all assets inside the network and helps identify threats. Without this visual map, the bank will be managing its cyber risks in the blind.

What the Board Should Do

Here are five steps that boards should take to remain proactive regarding information security.

- Review cybersecurity at every board meeting. Cybersecurity must be handled as a strategic boardroom issue, not as a back-office IT issue.

- Use the new information security exam procedures to perform a self-assessment. Identify and eliminate any deficiencies well in advance of the next exam.

- Review the network visibility map at every board meeting to visually identify all assets and the risk mitigation in place to protect them.

- Task a “hunt” team to identify anomalies within the bank’s network, as described in the new exam procedures. On average, attackers roam inside the network undetected for more than 200 days. Eliminate the exposure using advanced analytics that can mine through millions of records and reveal the attacker and the entire exposure. Response must be prompt.

- Conduct ongoing but randomly scheduled social engineering and phishing simulation training to keep employee awareness heightened. Education can prevent employees from falling victim to real attacks and becoming the weakest link in the chain.

In March, the Consumer Financial Protection Bureau fined an online payment processor for engaging in unfair, deceptive or abusive acts and practices (UDAAP), due to its failure to implement an adequate information security program and protect consumer data. Other regulators have taken notice, and will not hesitate to assess enforcement actions for information or cybersecurity deficiencies using UDAAP or other enforcement tools available against banks and its technology providers. Information or cybersecurity lapses can cause irreparable harm to the bank, and tarnish its reputation instantly. The stakes are very high. Banks must stay one step ahead.

WRITTEN BY