Tim Kosiek

Your M&A Success Could Depend On This One Thing

Close

About the authors

Written by

Tim Kosiek

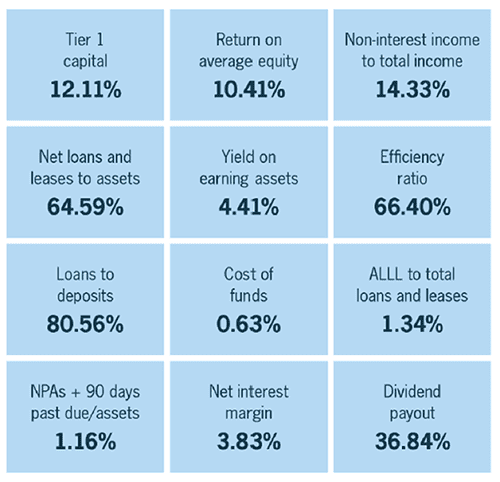

Benchmarking key performance indicators (KPIs) can help you more fully understand your bank’s financial condition and operating results, as well as the true value in a potential M&A market.

Benchmarking key performance indicators (KPIs) can help you more fully understand your bank’s financial condition and operating results, as well as the true value in a potential M&A market.

The success of your M&A strategy – whether buy, sell or stay – measurably increases with a sound grasp of the metrics that drive shareholder value.

KPIs as M&A drivers

KPIs can help you to identify important strengths in your target organization and your own institution. This can help determine the areas you could strengthen in an acquisition, or understand where your bank’s value lies within a merger. You can also learn about your organization’s, or your target institution’s, primary challenges and how this might impact the transaction.

These metrics can also help the organization evaluate the success of the transaction after completion. Have the key performance indicators drastically changed? Was that change different from the anticipated adjustment from the combination of the two entities? Understanding the metrics, and some of the forces impacting them, can be a strong foundation for successful M&A transactions.

Q3 2018 KPI observations

Community banks throughout the U.S. used the strong economy and relatively stable interest rate environment to maintain steady operations throughout the third quarter of 2018.

Baker Tilly’s banking industry key performance indicator (KPI) report reflected almost no change in comparison to the same benchmarks for the second quarter of 2018. Earnings, credit quality and capital adequacy benchmarks all remained essentially the same. This consistency appears to reflect a more stable economic environment, disciplined management of credit pricing and quality, notwithstanding a continued highly competitive environment, and the early stages of a move to higher interest rates.

If there is anything to take away from the relatively unchanged KPIs over the first nine months of 2018, it is that community bankers have diligently pursued the opportunities emerging from the strong economy.

Loan growth, reflected in the comparison of the loan-to-deposits ratios each quarter, has been somewhat subdued. Potential drivers of this include increasing liquidity pressures arising from changes in interest rates, early stages of the potential for a downward credit cycle and the uncertainty of the November midterm elections. These factors kept many community bankers focused on internal matters such as compliance and technology during the second and third quarters of 2018.

Many banks continued to assess consolidation opportunities on both the buy and sell side. Until the recent series of market declines, bank equity currency remained quite strong, supporting a continued active consolidation of the industry, at price points that, on average, exceed 1.5 – 1.7 times book value.

We expect more of the same consistency in the KPIs as we have seen throughout 2018. It does not appear there will be any significant shifts in either direction arising from changes in economic policy. However, the pace of deregulation may subside due to the change in leadership in the U.S. House of Representatives.

If equity markets rebound following the midterms and the Federal Reserve pauses its increase of interest rates, we may see a re-acceleration of the consolidation of community banks, especially those with assets of $500 million or less. Other than an increased emphasis on securing and maintaining low cost deposits, we anticipate community banks to maintain a steady course into early 2019.

WRITTEN BY