It goes without saying that 2011 was not a great year for banking. John Duffy, the vice chairman of investment bank Keefe, Bruyette & Woods, laid out the industry’s performance, such as it was, at Bank Director’s Acquire or Be Acquired Conference in Phoenix recently.

It goes without saying that 2011 was not a great year for banking. John Duffy, the vice chairman of investment bank Keefe, Bruyette & Woods, laid out the industry’s performance, such as it was, at Bank Director’s Acquire or Be Acquired Conference in Phoenix recently.

The industry is now well capitalized and non-performing loans are on the downswing, he said, but that doesn’t present the whole picture, and the whole picture is exactly what investors are looking at.

On a bright note, capital ratios have been rebuilt in the last three years, after declining from 2002 to 2008. The industry average tangible common equity to tangible assets is now 8.6 percent as of the third quarter, reaching a 70-year high, as banks have focused on rebuilding their strength and capital following the financial crisis.

Credit quality continues to improve, as non-performing assets to total assets dipped in the third quarter. However, Duffy said credit quality still needs to improve to get investors feeling better about the sector.

The total amount of nonaccruing loans, restructured loans and other real estate owned (foreclosures) ramped up starting in 2007 and remains high, at close to $350 billion in the third quarter for institutions insured by the Federal Deposit Insurance Corp.

New non-accruing loans increased in the third quarter by $26.3 billion, compared to an increase of $22.4 billion in the second quarter.

“The problems are taking longer to resolve than many people would have expected 12 to 18 months ago,’’ Duffy said. “If you’re looking just at non-performing loans, you’re probably not getting the whole picture. We’re seeing very slow progress in terms of the banks’ ability to move those off the balance sheets. The banks aren’t willing or able to move them off.”

He said investors are looking at that trend and not liking it.

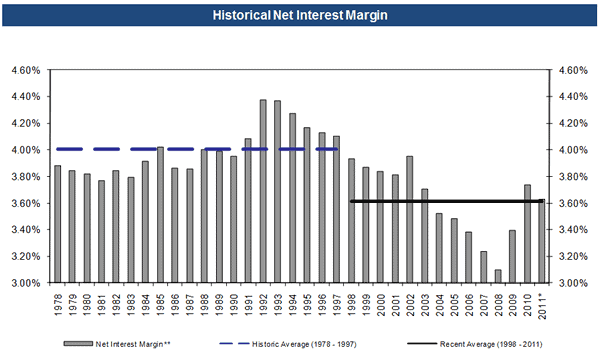

Interest rates are low and bank margins are getting squeezed, although net interest margin, at slightly more than 3.6 percent in 2011, isn’t as low as it was a few years ago. The average net interest margin for small to mid-cap banks, or those with less than $2 billion in assets, was 3.77 percent in the third quarter.

With all those headwinds, it’s no wonder that banks are trading at less than book value, Duffy said.

The banks that are trading below book value don’t have the profitability metrics or the capital to provide assurance to investors, he said.

“I’m not sure the industry is undervalued,’’ he said. “I don’t think the markets are irrational.”

He said investors are uncertain about the future, both in terms of profitability and capital demands from regulators.

The industry’s performance and investor reluctance has played out in the deal market as well. There were 163 bank mergers and acquisitions in 2011, down from 178 the year before and 288 in 2007, he said.

The median price to book value last year was 100 percent, down from 112 percent in 2010 and down from a 10-year high of 220 percent in 2006.

The median core deposit premium paid was just 0.3 percent last year, down from 19.7 percent in 2006, showing that buyers value deposits much less than they had in the past.

Duffy says there is still a lot of opportunity for M&A, as 844 banks remain on the FDIC’s list of troubled institutions. There are 446 banks as of the third quarter with a Texas ratio of greater than 100 percent, an industry metric that often points to future bank failure.

“There are still many more failures to come,” he said.