Paul Weinstein Jr.

Optimistic About Loans But Worried About Deposits

There are a lot of reasons why Greg Steffens is confident about the economy. As the president and CEO of $1.8 billion asset Southern Missouri Bancorp, which is headquartered in the southern Missouri town of Poplar Bluff, he sees that consumers are more confident, wages are growing, most corporations and individuals just got a tax break, and the White House announced a major infrastructure funding plan.

There are a lot of reasons why Greg Steffens is confident about the economy. As the president and CEO of $1.8 billion asset Southern Missouri Bancorp, which is headquartered in the southern Missouri town of Poplar Bluff, he sees that consumers are more confident, wages are growing, most corporations and individuals just got a tax break, and the White House announced a major infrastructure funding plan.

Steffens projects that a strong local economy will help Southern Missouri to grow loans by 8 to 10 percent this year. But he sees the potential for net interest margin compression as well, particularly because competition for loans and deposits has gotten so tight.

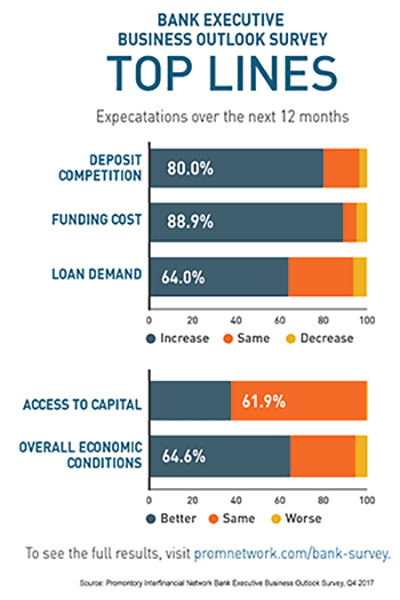

His thoughts about the future, a mixture of optimism and concern, are typical of bankers these days as shown by Promontory Interfinancial Network’s latest Bank Executive Business Outlook Survey. Although bankers report higher funding costs and increased competition for deposits, their optimism about the future has improved, and economic conditions for their banks are better now than they were a year ago.

Along with a generally improving national economy and improvements in the banking sector, the passage of the Tax Cuts and Jobs Act shortly before the survey was taken likely influenced the increase in optimism among many bankers. The emailed survey, conducted from Jan. 16 through Jan. 30, included responses from bank CEOs, presidents and chief financial officers from more than 370 banks.

Along with a generally improving national economy and improvements in the banking sector, the passage of the Tax Cuts and Jobs Act shortly before the survey was taken likely influenced the increase in optimism among many bankers. The emailed survey, conducted from Jan. 16 through Jan. 30, included responses from bank CEOs, presidents and chief financial officers from more than 370 banks.

Some highlights include:

- Sixty-three percent say economic conditions have improved compared to a year ago, while 5 percent say things have gotten worse, compared to 49 percent last quarter who said conditions improved and 9 percent who said things had gotten worse.

- Slightly more than 58 percent report a recent increase in loan demand, up 7.5 percentage points from last quarter.

- Bankers think the future will be even better with 64 percent projecting an increase in loan demand in 2018, compared to just 51.2 percent who projected annual loan growth in the fourth quarter 2017 survey.

- The Bank Confidence IndexSM, which measures forward-looking projections about access to capital, loan demand, funding costs and deposit competition, improved by 2.4 percentage points from last quarter to 50.5, the highest rating for the index since the second quarter of 2016.

- Regionally, the highest percentage of bankers expecting loan growth is from the South at 71.9 percent. But the biggest improvement in expectations for loan growth is in the Northeast, which climbed 27.1 percentage points from last quarter to 64.1 percent expecting loan growth in 2018.

Charlie Funk, the president and CEO of MidwestOne Financial Group, a $3.2 billion asset banking company in Iowa City, Iowa, says he expects the tax cuts will lead to higher commercial loan growth, although he hasn’t seen evidence of that yet.

He’s worried now about another factor on his balance sheet: deposit competition. “Deposits are going to be where the major battles are fought,’’ he says. The bank already is paying some large corporate depositors more than 1 percent APR on money market accounts, compared to 30 basis points just after the financial crisis. He expects the bank’s net interest margin to narrow somewhat this year as deposit costs increase faster than loan yields.

Other bankers report higher levels of deposit competition as well. In the Promontory Interfinancial Network survey, 80 percent of respondents expect competition for deposits to increase during the year, compared to 77.4 percent who thought so last quarter. The overwhelming majority have seen higher funding costs this year at 78.1 percent, compared to 68.4 percent last quarter who experienced higher funding costs. Nearly 89 percent of respondents expect funding costs to increase this year.

Representatives from larger community banks, with $1 billion to $10 billion in assets, were more likely to say funding costs will increase. The Northeast had the highest percentage of respondents saying funding costs will moderately or significantly increase, at 92.3 percent.

One of those Northeastern banks is Souderton, Pennsylvania-based Univest Corp. of Pennsylvania. With $4.6 billion in assets and a 100 percent loan-to-deposit ratio, the highly competitive deposit market is putting pressure on the bank to match loan growth with deposits. Univest Senior Executive Vice President and Chief Financial Officer Roger Deacon says funding costs have inched up, partly driven by competition for deposits. “The competition is almost as high on the deposit side as on the loan side,’’ he says.

The good news is that the bank is asset sensitive, meaning that when rates rise, its loans are expected to reprice faster than its deposits. “I’m cautiously optimistic about the impact of rising rates on our business,’’ Deacon says.