Rick Childs

Partner

Enter your email address and password below to gain access.

Rick Childs is a partner at Crowe LLP. He has over 35 years of experience in business valuation, transaction advisory services and accounting for financial services companies. Mr. Childs is the national practice leader overseeing the delivery of transaction and valuation services to the firm’s financial institutions clientele. His business valuation experience includes ASC 805 purchase price allocations including a focus on loan valuations, ASC 350 goodwill impairment testing and valuation of customer relationship intangible assets, including core deposit intangibles.

Mr. Childs is a frequent presenter for both national and state professional organizations including the SNL Financial, Bank Director, AICPA and Financial Managers Society. He has published articles on mergers and acquisitions in the ABA’s Commercial Insights, Community Banker, Bank Director and Bank Accounting & Finance.

The most-often recorded and identifiable intangible asset for a bank or branch acquisition is the core deposit intangible (CDI). When valuing CDIs, banks should make sure to value those deposits using the actual market value, rather than the deposit premium paid. This article will explain how to determine the actual market value.

A CDI asset arises when a bank has a stable deposit base comprised of funds associated with long-term customer relationships. The CDI value derives from customer relationships that provide a low-cost source of funding. CDIs are common assets, as most banks have some level of stable depositors to whom they pay interest at a rate lower than the rate they would pay alternative funding sources.

Core Deposit Values

Valuing CDIs is difficult because they sell only with the group of deposits that give rise to them. A bank should determine the market price of a CDI by aggregating data on CDI values as reported by banks in their annual and quarterly filings.

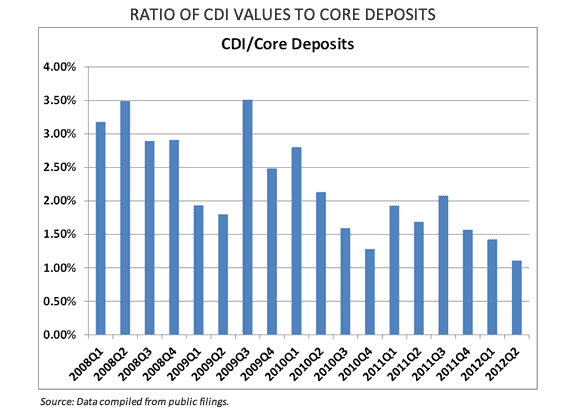

Using publicly available data on completed whole bank transactions for the period of Jan. 1, 2008, through July 1, 2012, we compiled the values for the CDIs.

To calculate the ratio of CDIs to core deposits, we aggregated the following deposit types to compute the bases:

As shown below, CDI values have declined over time as interest rates have declined during the same time frame. The chart includes data from the banking organizations on amortization and useful life, or the time period an asset is expected to contribute directly or indirectly to future cash flows.

Useful Lives and Amortization Methods

FASB provides guidance that if an income-based method is used to develop the value of the intangible asset, the period of projected cash flows should be considered when choosing a useful life.

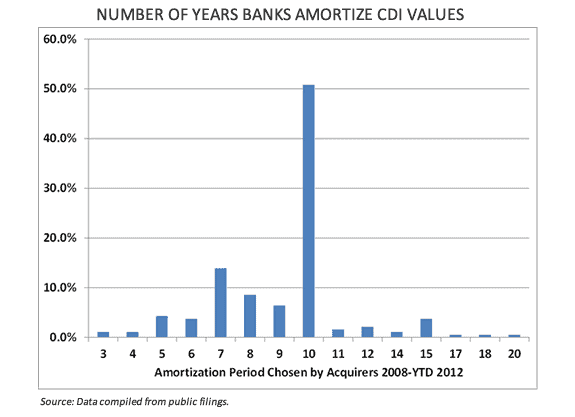

It’s not uncommon to find deposit relationships that have very long lives. So how does a bank choose a useful life, especially when there might be deposit relationships with lives significantly longer than the average life of the acquired deposit relationships? One source of guidance comes from the Office of the Comptroller of the Currency (OCC), which publishes the Bank Accounting Advisory Series on various accounting issues. In its most recent guide, the OCC indicated that in most cases the useful life for CDI wouldn’t exceed 10 years, although exceptions could be possible. Because banks file call reports on the basis of U.S. generally accepted accounting principles, the ultimate decision rests with the bank in consultation with its external audit firm.

The following chart shows that the majority of acquiring banks took the regulatory guidance to heart and chose 10 years as a useful life.

The method of amortization is another important component of recognizing expense related to CDI through the income statement.

The method of amortization for any finite-lived intangible asset is influenced by ASC 350-30-35-6, which states that “the method of amortization shall reflect the pattern in which the economic benefits of the intangible asset are consumed or otherwise used up. If that pattern cannot be reliably determined, a straight-line amortization method shall be used.” Since 2008, the majority of acquirers have chosen a method consistent with the pattern of economic use and not straight-line amortization, likely because an income-based method that models attrition in deposit relationships can better show economic patterns.

Rick Childs is a partner at Crowe LLP. He has over 35 years of experience in business valuation, transaction advisory services and accounting for financial services companies. Mr. Childs is the national practice leader overseeing the delivery of transaction and valuation services to the firm’s financial institutions clientele. His business valuation experience includes ASC 805 purchase price allocations including a focus on loan valuations, ASC 350 goodwill impairment testing and valuation of customer relationship intangible assets, including core deposit intangibles.

Mr. Childs is a frequent presenter for both national and state professional organizations including the SNL Financial, Bank Director, AICPA and Financial Managers Society. He has published articles on mergers and acquisitions in the ABA’s Commercial Insights, Community Banker, Bank Director and Bank Accounting & Finance.